Generally, loans are made (and money is created) for one of three purposes:

The first of these purposes is positive and essential, the other two are not. If you buy shares in a company when they are first issued, or if a bank lends money to a firm so it can expand, the money invested will be used to increase productivity or efficiency. If the firm is clever with the investment, it should sell more goods and increase its rate of profit. Investors will be rewarded with dividends and new and existing employees will benefit from increased wages. A virtuous circle emerges as money circulates around the economy, ensuring more demand for the goods produced by this firm and others. All in all, a positive impact is made on the economy. This form of direct investment in enterprise is essential, and the returns earned from it are entirely legitimate.

But currently in the UK only eight per cent of bank loans are made for investment in productive enterprise.

Loans for investment in secondary markets for stock and shares, in the bond markets, in the currency markets or in markets for financial derivatives, have no direct link to productive enterprise. They are not part of the real economy. Neither are investments made in raw materials or commodities if the purchase is not to secure inputs for manufacture. Such investments are made in the hope, or calculation, that the ‘asset’ in question will rise in value and so deliver a tidy return. That eight per cent is still quite a lot of money. It should have a positive impact on both the creation of wealth and its distribution. But, even if the return on investment is divided fairly among the factors of production and labour receives a just wage, there is still a problem.

Because the other ninety-two per cent of bank-created money produces no additional wealth, it contributes to the debasement of the currency.

The wage-earner may have more money in her pocket, but as prices have gone up she is no better off. The process of creating money causes a redistribution of wealth from the bottom to the top of the earnings pyramid, and the gulf between rich and poor gets bigger and bigger.

Most of the funds for such speculative investment begin life as loans. Money is often created by one division of a large bank and loaned to another to play the markets. No investment is made in the generation of real wealth, but large amounts of debt are constantly being created which destabilize the real economy. If this kind of speculative investment creates no new wealth, then any return it earns for investors must be derived from money created out of nothing, or from the earnings of those who are involved in the production of genuine wealth. This activity is called rent seeking.

The third type of loan – those made for consumption – need not be economically crippling if they are limited. Currently they are not. In the UK, personal debt is roughly equal to the entire annual output of the economy. Mortgages account for eighty-five per cent of that debt; but when non-mortgage consumer debt is more than £8,000 per household, rising to £15,000 if you exclude households with no debt, you begin to see the size of the problem.

Many households are spending way beyond their means, either because the breadwinner is unemployed or poorly paid, or because their consumption outstrips their earnings. Some of that consumption is perfectly justified – nobody can be blamed for borrowing money to feed and clothe their children – but most is fuelled by a destructive culture which tells us we can have all that we want regardless of what we can afford.

Promoting consumption for its own sake is a way of diverting people’s attention from what’s really going on in the world.

The dire consequences of a debt-driven economy could be avoided if consumer credit wasn’t so easily available. With so much manufacturing now transferred to emerging economies, where wages are lower, most of the money lent for consumption in rich countries ends up funding imports and is lost to the domestic economy for good. If, instead of funding consumption, the loans were used for investment in productive enterprise, then companies could take on new staff, and demand for locally produced goods (that don’t need to be transported halfway round the world) would begin to grow.

If loans were extended only for the purpose of creating genuine new wealth, many of the problems associated with money supply instability would disappear. Perhaps this is unrealistic, as it would require a complete overhaul of the banking system, but it would address a fundamental economic problem. As economist Dr Michael Reiss says, “the history of economics has been a history of mankind’s attempts, and mostly dismal failures, at establishing and sustaining a stable monetary system.”

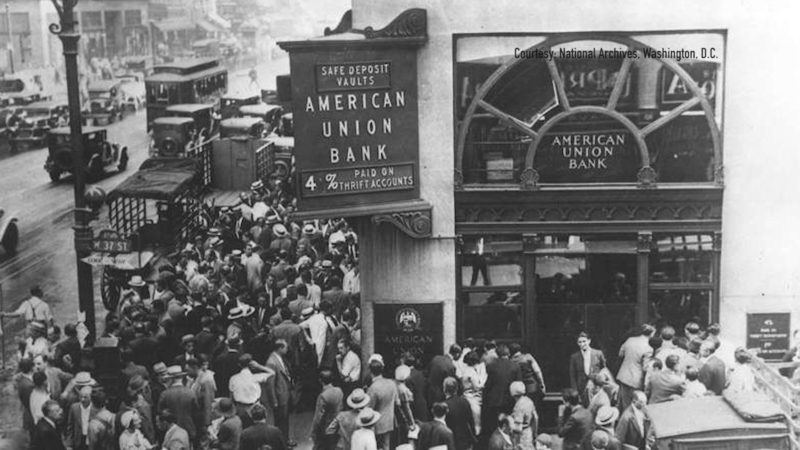

And, nearly a century after the failure properly to police the gold standard created the conditions that led to the Wall Street Crash, bankers have again escaped regulation and wrought havoc on the global economy by manipulating the money supply.

Why has it proved so difficult to maintain a stable money supply? Because the manipulation and corruption of the system by which money is issued has always been one of the easiest ways for predatory individuals and corporations to make a fast buck.

A stable money supply would mean everyone having to work for a living, doing something that actually adds value and creates real wealth. This is the kind of work from which most people derive meaning and purpose in life. Regardless of the consequences for the rest of society, it seems that bankers, and others who play the financial markets, have a different motivation. They seem determined to go on making money without creating anything of genuine value.

Excerpt from Four Horsemen: The Survival Manual.

Could this be the year that sends the silver price to the moon and gives the so-called silver stackers their long awaited moment in the sun?

The Great Reset agenda seems to be losing steam and those in charge of implementing it are losing conviction.

The Corona pandemic has exposed the glaring fault lines of some of the world's most clunky and inefficient banking systems.