Most people equate money with wealth, but in economic terms money and wealth are quite separate things. Wealth can be defined as those goods and services which are essential to wellbeing, along with others which enhance our experience of life. Money can be used to acquire such wealth, but of itself money is not wealth. This is a crucial distinction, but one about which neo-classical economics has very little to say.

Money is a means of exchange; it enables us to secure wealth. It helps facilitate the processes of extraction, production and trade through which human beings convert the planet’s natural resources into the things we want and need. It can be used to acquire any of the three factors of production, land, labour and capital, but it is not a factor of production in the same way. Depending on how money comes into existence, however, it can have a serious impact on the creation and distribution of wealth. Economists should take this into account, but generally they don’t.

Keynes was aware of the role of money in the economy, especially its destabilizing qualities, though, as Steve Keen says, “he failed to convince his fellow economists of the importance of money in modelling the economy because money didn’t feature heavily in his technical analysis.” And, to the neo-classical economist, technical analysis is everything.

Economic activity isn’t just a question of people working, alone or in groups, to convert the gifts of nature into things that are useful or that bring pleasure; it is also a matter of exchange through trade. In a purely agricultural economy, life would be pretty dull if we each produced only a single crop to consume at every meal. Adam Smith taught us that the basis of a modern economy is the specialization of labour, and trade between the producers of manufactured goods and consumers of those goods. This enables us to satisfy our needs and desires by acquiring a variety of goods and services in the marketplace. Trade is an integral part of all societies; it reflects a universal appetite for variety in what we consume. There is nothing more natural or instinctive than engaging in trade so that we can enjoy the fruits of other people’s labour in exchange for a share of our own. To enable trade we need money, so we can price goods and services in terms of each other and exchange the wealth we each create for wealth created by others.

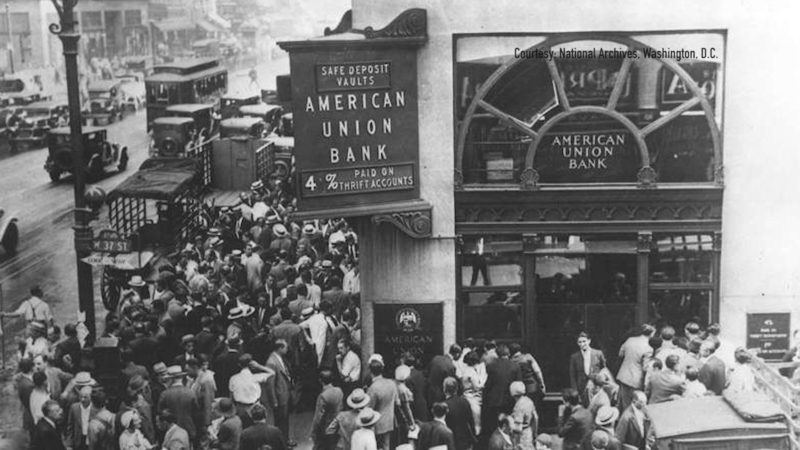

History shows that economic instability, and ultimately civilizational collapse, is closely linked to wild fluctuations in the quantity of money in circulation, and to changes in its value. By ensuring stability of the money supply, the amount of money in circulation, we are better able to protect ourselves from such problems. The only other acceptable use for money is as a temporary store of value, a means of deferring consumption to a later to a later date– to sustain us in old age, for example. If we are to use money as a temporary store of value, then it’s crucial that money keeps its value over time. Inflation occurs when money loses its value, leading to the same quantity of money buying less wealth. Most of us have personal experience of this.

Excerpt from Four Horsemen: The Survival Manual.

Could this be the year that sends the silver price to the moon and gives the so-called silver stackers their long awaited moment in the sun?

The Great Reset agenda seems to be losing steam and those in charge of implementing it are losing conviction.

The Corona pandemic has exposed the glaring fault lines of some of the world's most clunky and inefficient banking systems.