While our deliberately deregulated, debt-laden economy was always headed for a fall, the fuse for the wider crisis was lit by ‘sub-prime’ mortgage lending in the United States. Mortgage lenders had taken unprecedented risks in making loans for home purchases to people who would never be able to repay them.

Such loans would not previously have been made, but, as Michael Hudson points out, around the turn of the millennium, in their relentless quest for new sources of profit, bankers began to realize that “the poor are honest”. They will do everything they can to repay their debts “even if the debts are not valid; even if the debts are much more than they expected; even if they really can’t repay the debts.” And the poor cannot afford lawyers.

Having indebted credit-worthy Americans to the hilt, the money men set about foisting debt on to the seriously credit-unworthy. Predatory lending terms were hidden in the small print of confusing mortgage contracts. Lenders (whose pay and bonuses were linked to the amount of business they did) encouraged people to take out loans with low ’teaser’ interest rates, which soon increased beyond affordability. Almost all sub-prime borrowers were unaware of what they we committing to. And, as Hudson points out, there were worrying racial undertones to the whole sordid business: “The banks engaged in a criminal conspiracy to charge more to the blacks and Hispanics.”

The boom years, and subsequent collapse, were driven by a very simple mechanism: lending became a ‘production-line’ process. Large quantities of money (created out of thin air) needed to be unloaded on to unwitting borrowers.

This practice of ’mortgage mining’ made unscrupulous use of the manipulative emotional propaganda that underpins the American dream.

The bankers struck gold. In the late nineties they convinced government and regulators to look the other way. The ‘free market’ would deliver the American dream to every citizen; nothing could possibly go wrong. There were a few canaries in the mine who warned of the consequences, but they were dismissed as cranks and conspiracy theorists.

John Lanchester describes the situation thus: “A terrible changeover happens, in which the process of lending is no longer driven by the legitimate desire of poor-but-reliable people to own a house, but is instead a manufactured process driven by capital which is set loose looking for people to sign up to loans.” As Simon Johnson says, “if you push people to buy housing before they are ready, if you push very dubious loans on them, and they don’t understand what they are getting themselves into, you can have huge adverse repercussions.”

Apart from the pathological desire for profit, lenders were able to make these dodgy loans because of the emergence of a thriving new market in mortgage debt. Banks and other players in the financial markets began trading packages of mortgage debt to swell their profits and bonuses. Many had no idea of the origin or validity of the loans that made up these ‘securities’ but the existence of a thriving market was security enough. For those making the initial deals, what started out as risky loans quickly became risk-free as the debts (and the risk) were sold on at a profit.

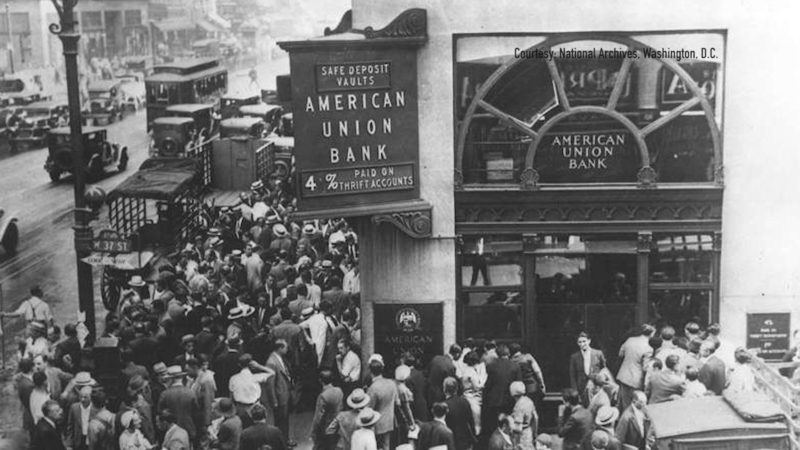

The markets eventually realized that the complexity of such ‘products’, and the complete lack of transparency regarding their provenance, meant nobody had any idea whether the underlying assets (homes) had any tangible value. Before long, the market for mortgage-backed securities was operating under the ‘greater fool’ theory: the belief that a dubious investment can be sold on to a ‘greater fool’ for more than you paid for it. Investing on the basis that packages of debt can be sold on at a profit is hardly a sound strategy. As the victims of inappropriate lending began to default on their mortgages, the greater fools began to wise up. But it was already too late. Confidence collapsed, the crisis kicked off and taxpayers worldwide were left to pick up the tab.

The real victims of the sub-prime scandal are the people who lost their homes. In Baltimore, a city where 50,000 homes already lie empty, more than 30,000 sub-prime borrowers have suffered foreclosure. Tens of thousands of people have no work and nowhere to live in a city full of empty houses.

The moral corruption of the financial system is almost beyond imagination.

Hiding predatory lending practices in the small print of complex financial products was only ever going to enrich one set of interests, and it was always destined to bring down the entire global economy.

Excerpt from Four Horsemen: The Survival Manual.

Could this be the year that sends the silver price to the moon and gives the so-called silver stackers their long awaited moment in the sun?

The Great Reset agenda seems to be losing steam and those in charge of implementing it are losing conviction.

The Corona pandemic has exposed the glaring fault lines of some of the world's most clunky and inefficient banking systems.