Economist Dr Steven Hail on how Japan has managed to avoid another financial crisis without creating a major private debt problem, while America and Australia… have not.

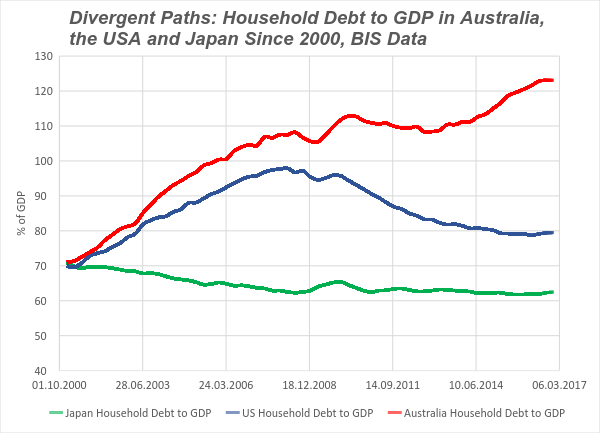

In the year 2000, Japan, the USA and Australia all had about the same ratio of household debt to GDP - in each country, this figure was about 70%.

In Japan, the ratio fell gradually from 70% to the low 60%, and has remained at about 62% for a while.

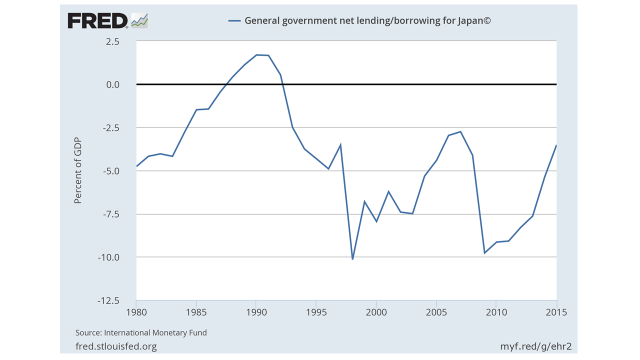

Admittedly Japan has had a current account surplus with the rest of the world on its balance of payments, while Australia and the USA have not. But the main reason the Japanese have managed to support their economy and at the same time avoid rising household debt has been a willingness to run government deficits. Over the last ten years, the Japanese fiscal deficit has averaged above 6% of GDP, but going back further, there has been a deficit ever since the Japanese financial crisis of the early 1990s.

The beneficial role of the deficit, and the irrelevance of its impact on the stock of Japanese government debt, is not generally understood, even in Japan. Debt and deficit in Japan are not a sign of economic failure – they are the hallmark of a largely successful attempt to maintain living standards and close to full employment labour market, in an economy where private saving (and especially corporate saving) has outstripped private investment spending.

It is very important to understand this. Many economists, commentators and credit ratings agencies still don’t understand this. They have been vaguely forecasting doom, or at least some kind of financial crisis, for Japan for a couple of decades now. It wasn’t in Japan that the Global Financial Crisis developed. It wasn’t in Japan that the problems of the euro emerged. It isn’t Japan that is faced with dangerous household debt now. These various commentators still don’t understand the fiscal space enjoyed by monetary sovereigns like the Japanese government. They don’t understand the appropriate role for the government’s budget in such countries. They look for crises where none will occur. They miss the financial fragilities which drive those crises that do happen. They are very slow to learn. The only thing to do is to ignore them and their advice.

In the US, household debt surged as financial fragility grew, with the ratio peaking at 98% in the first quarter of 2008. Households deleveraged post GFC, and the ratio fell back to about 80%. Still way too high for another surge in private debt to be allowed to persist, but at least well below its level at the peak of the bubble. Substantial government deficits in 2009, 2010 and 2011, and an average deficit of about 5% of GDP has made this possible, while providing enough support for demand to allow for a degree of economic recovery. The US fiscal deficit should have been higher for longer, and is much too low at the moment, But at least the household debt ratio has fallen somewhat.

What about Australia? Like Japan and the US, our household debt to GDP stood at about 70% at the millennium - well above the levels of previous years. It then grew and grew, mainly due to increasing mortgage debt, standing at 108% in mid-2008. Well above the level in the US when the crash happened there.

As we know, Australia missed the worst of the GFC, and propped up its housing market, and household debt just kept growing.

By the end of last year it was above 123%, placing Australia very near the top of the global league table.

Bound to lead to a crash? Many would say so – Steve Keen and Philip Soos amongst them, and who am I to disagree?

Unwise? On that we should all agree.

And done at the urging of successive governments which have failed to run appropriate fiscal policies; with the approval, for most of this period, of the RBA; and with the acquiescence of what until quite recently was a very relaxed APRA.

Who has the debt problem?

Not Japan.

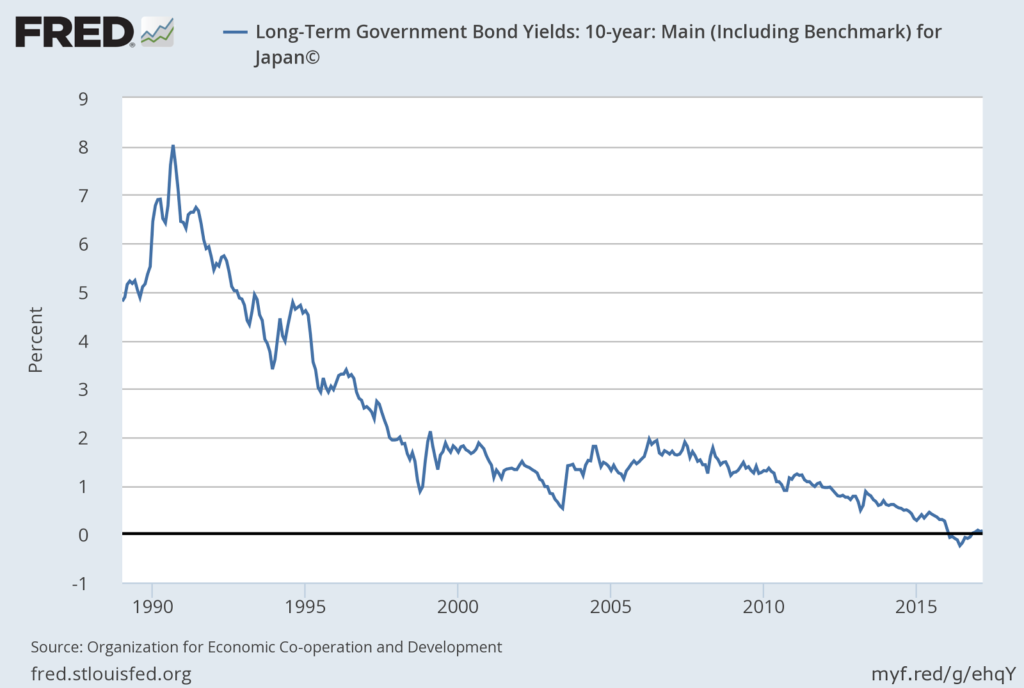

Since around 2013, The Bank of Japan began buying up government debt, to become a monopoly supplier of bank reserves, denominated in Yen.

In September 2016 it took the decision to buy unlimited amounts of Japanese government bonds at a fixed-yield, meaning it could control yields across bond maturities from a two-to-40-year output and sets them at whatever level they choose. It also implemented $80 trillion worth of quantitative and qualitative easing while introducing a negative interest rate of minus 0.1% to current accounts held by financial institutions at the bank, driving the bond yield rate down. Bond market dealers queued up to get their hands on as much Japanese government debt as they could, with the promise it would mature within 40 years.

To quote Economist Bill Mitchell: “The bond markets do not have the power to set yields unless the government allows them that flexibility. The government rules, not the markets.”

Moreover, Japan’s government doesn’t need to issue debt in primary markets in order to spend.

Because monetary sovereign government debt is not the problem.

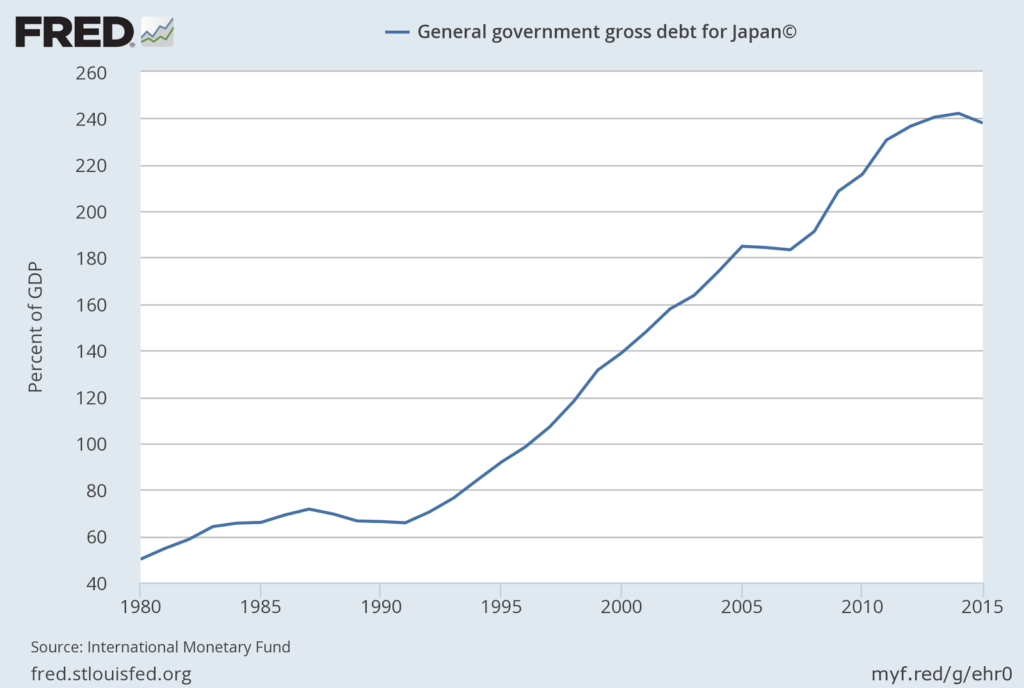

The chart below can always be used to scare those who don’t understand monetary sovereignty, and the fact that government debt is just non-government saving, but if you understand the fiscal space available to governments like those of Japan, the USA and Australia, you know that government debt ratios, taken out of context, are irrelevant.

There can be no government debt crisis in these countries. Government debt is better thought of as a form of money, and not debt in the conventional sense at all.

Don’t be intimidated by the dizzy heights of Japanese government debt. It isn’t in itself inflationary.

It doesn’t imply in itself imply higher interest rates.

It has helped to keep Japan close to full employment, when the Japanese private sector has been saving rather than investing.

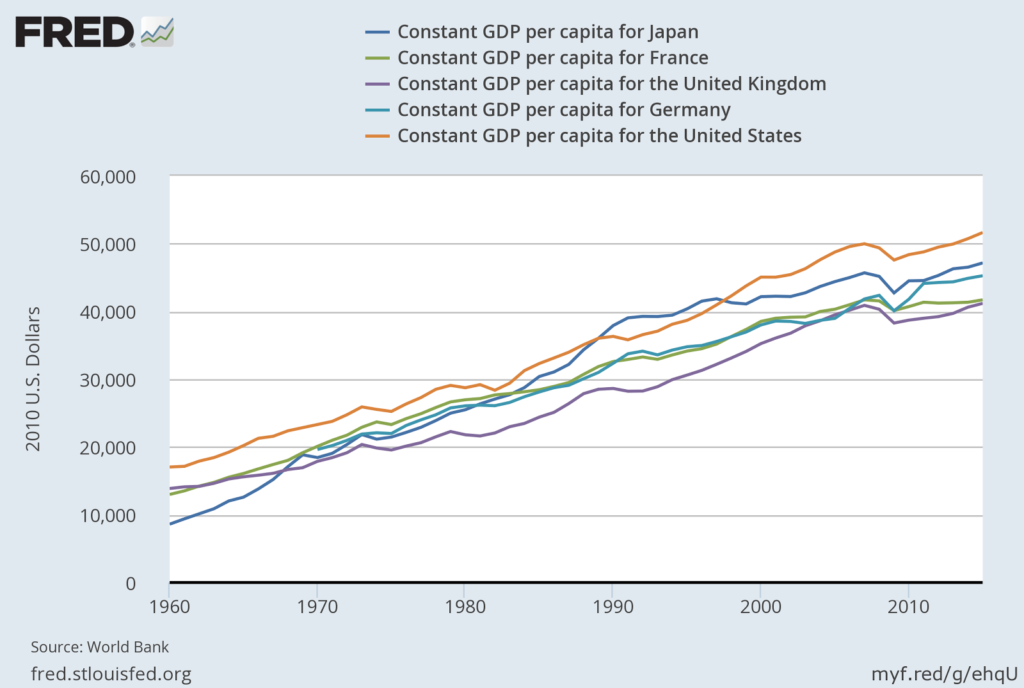

And Japan hasn’t done so badly in terms of income per head either. The economy may not have grown rapidly, but the population has been shrinking. In terms of productivity and GDP per capita, Japan has been doing pretty well, given its ageing population.

Australia too has performed relatively well in terms of GDP per capita, but has relied more on household debt and less on government debt. So despite its better demographic prospects, it is Australia which is faced with the debt problem – not Japan.

Household debt is the problem.

The Australian government was running a fiscal surplus in the run-up to the Global Financial Crisis, relying on a mix of mining investment and household debt to grow its economy. Even after the crisis, the fiscal deficit was neither large enough nor maintained at a high enough level for long enough, to permit an economic recovery with falling household debt. Instead, successive governments placed their bets on an ever-inflating property market and on a household debt bubble which would never burst.

They still haven’t learned what monetary sovereign government fiscal policy should be all about. They still don’t understand government budget deficits are not really borrowing at all, and that monetary sovereign government debt is not really debt in the conventional sense. They behave as though the government can become insolvent, or otherwise might cause hyperinflation. They are completely wrong.

Who has the debt problem?

Australia. And America.

Because monetary sovereign government debt is not the problem.

Household debt is the problem.

Dr Steven Hail

Dr Hail holds a BSc and an MSc from the London School of Economics, in addition to a PhD from Flinders University.

How do you spend your days?

I spend my weekdays teaching financial economics at the University of Adelaide, and my weekends mostly in the Adelaide Hills.

Why is economics important to you?

Economics is important because in the end economists, for good or ill, rule the world. At the moment, it is largely for ill, because the economics profession has become increasingly dominated by the ideas of economists who misunderstand and misrepresent how the economy works, and even what governs human and social well-being. To make genuine progress towards building sustainable and equitable societies, we have to take economics back these people. This is vitally important. As Keynes' says, at the very end of his 'General Theory', "the ideas of economists and philosophers, both when they are right and when they are wrong, are more powerful than is commonly understood. Indeed the world is ruled by little else. Practical men, who believe themselves to be quite exempt from intellectual influences, are usually the slaves of some defunct economist". And as Hyman Minsky said, in 1986 in his great work, 'Stabilising an Unstable Economy', "The game of policy making is rigged; the theory used determines the questions that are asked and the options that are presented. The prince is constrained by the theory of his intellectuals." The defunct economists are in control of the options presented to policy-makers at the moment, and there are a series of questions that are not being asked and options that are not being presented to policy makers, because they are listening to defunct economists, and are not even aware that there is another better way of thinking about the economy.

What drove you to focus on economics. Was there a particular moment you can remember that led you to this field?

As an adolescent, I wanted to understand the reasons for the rise of Thatcherism, and the causes and likely consequences of the changes going on around me in the UK. I think the election of the Thatcher Government in 1979 was the single biggest motivating factor for me to study economics.

What drives you professionally?

I enjoy my job. I don’t need anything to drive me, beyond that. I am a teaching specialist, and my job is to share an understanding of realistic macroeconomics and finance with as many students as possible.

In your opinion what are the three biggest problems facing the developed and developing world?

(1)Climate change (obviously)

(2) The fact that most of the economics profession, almost all politicians, almost all journalists, and almost the whole of the engaged public completely misunderstand macroeconomics, leading to unnecessary underemployment and relative poverty, excessive private debt and frequent financial crises.

(3) The prospect of further wars and terrorism, encouraged in part by the consequences of (2) and increasingly also by the consequences of (1)

If you hadn’t become an economist, what would you have done?

Been a maths teacher.

What led us to this moment in history?

The persistent and successful promotion and pursuit by the Right of a particular way of organising the economy and society, starting in the 1950s, but with sustained success only since about 1980. The craven submission and surrender of the establishment Left, which has more or less en masse accepted the disastrously misleading frame used by the Right for generating and evaluating policy proposals. The tame co-operation of journalists and other commentators in what has now been a long period in which the public have been gradually brainwashed into thinking there is no alternative to what has become known as neoliberalism.

What are the lessons we failed to learn during and since the 2008 crisis?

Fiscal policy works. Governments that issue their own currencies can’t become insolvent in those currencies. Monetary policy doesn’t work, Economies relying on private debt and bubbles in property and/or share prices to grow demand and pursue full employment will eventually face a severe recession. The approach used to manage economies since the early 1980s eventually created a very fragile financial system, and won’t work any more. There will be no return to the pre-2008 ‘normal’ times.

Can you list some ‘Baby Steps’ out of the current economic mess?

Stop talking about a ‘return to surplus’, and shift your concern away from government debt (which isn’t really debt in the conventional sense at all) and towards household debt. Start regulating banks and financial markets properly. Introduce a job guarantee, along the lines suggested by people like Bill Mitchell, at the University of Newcastle in NSW, and Pavlina Tcherneva, at the Levy Institute in New York.

If you were a global President what would your first three pieces of policy be?

To dissolve the world government, as it won’t work. That is the last thing we need. Then I would not be global President any longer, so there would be no need for two further pieces of policy.

Tell us something you have been wrong about?

Spoiled for choice. I used to be, until 10-15 years ago, a largely uncritical teacher of neoclassical (neoliberal) economics. I had started off as an idealist, but (like so many students down the decades) was brainwashed by the single school of thought presented to me, while at university. It took years for me to realise there is more than one school of thought regarding the way capitalist economies work, and that the modern orthodox neoclassical way of looking at the world has rotten foundations and is in many ways disastrously misleading. I try to be compassionate to those still thinking within a neoclassical frame, because for a long while I was one of them, and I know how very hard it is to escape that frame. In some words of Keynes, written in December 1935, ‘the difficulty lies, not in the new ideas, but in escaping from the old ones, which ramify, for those brought up as most of us have been, into every corner of our minds.’

You are stuck in a ski lift for twenty four hours - you can have one person (living or dead) with you who will it be?

My late mother. Sorry – not interesting, but true. If forced to pick someone else, it would be John Maynard Keynes. Predictable perhaps, but it would. (1) Mum (2) JMK. Perhaps I could have them both there. We’d have a great time of it.

Name the book that changed you….

On Being a Christian, by Hans Kung.

This is the book which finally convinced me I was (and am) an atheist.

What would you do differently if you were to start all over again?

Move to Adelaide sooner. I left London in the year 2000. Wish I’d come here in about 1990.

Give our readers, members and subscribers a piece of advice that has served you well… Anything you would like to plug? Now is your chance.

The best piece of advice I have ever received is to have limited expectations about changing the world for the better, but to keep trying anyway. I have never voted for the winning side in a general election in the UK or Australia. It would be easy to be discouraged. But it is important to me to retain a sense of purpose, and even if making genuine progress is a very long game, to at least do my best to be helpful, and to not be remembered as a flat-earther (which is how many of today’s most prominent orthodox economists will be remembered in the decades to come).

I encourage everyone to take an interest in modern monetary theory. An easy way of doing this is to watch the many presentations by and interviews given by Bill Mitchell, Stephanie Kelton, Warren Mosler and Randall Wray.

Latest posts by Dr Steven Hail (see all)

- Why have wages been allowed to stagnate? - January 4, 2018

- A just social-wage and a job guarantee - December 28, 2017

- Household Debt: A Tale of Three Countries - July 18, 2017

Interesting article. Don’t know if MMT will work most places, as gov’ts are massively corrupt. Huge amounts of printed money go to banksters. In the U.S. both parties have refused to work together for years. Spend their time making up issues that take all their time. They have no time left to solve problems, like health care and education.

Incentivising jobs is good, but companies don’t really want employees, they have been automating jobs for years. Look at auto mfg. There are far fewer workers in auto plants. This same thing is happening in most industries, that is why we have so many unemployed. Oh, make that marginally detached, gov’t doesn’t like the term unemployed, so they don’t count them.

Big corporations own Washington. Gov’t does little to subsidize or incentivize small business, but throws billions at big companies. If you get a job overseas, you have to pay taxes on that income. If a big company has foreign subsidiaries, they don’t pay taxes on that income. So, Apple has about $250 billion that has not been taxed. Politicians never seem to be able to solve these problems but they are all over foreign campaign meddling. Whose watch did this happen on anyway?

Are they working to solve the problem, or just jawing about it? No progress made on important issues.

Also, need to get people to stop taking out so much debt. Don’t know if higher interest rates are the only answer.

How do we get people to change this behavior? Clearly, household debt is a major cause of recessions and market crashes.

Public unions are making health care and education unaffordable. Look at Chicago.

Don’t know the solution to that.

But it is not just me that does not have a solution to these problems. No one seems to.

It will be very difficult to provide guaranteed jobs, because they will intersect union work everywhere. We could have people on public assistance do some work, but it would likely be taking union work somewhere. In Michigan a union is suing over goats taking their jobs, at Western Michigan University. Gonna be tough to give people work.

The U.S. has become a very inefficient society. Too many people not working. Too many people in inefficient service jobs.

I think it is going to take more than fiscal stimulus to solve these problems.