Fractional reserve banking began in Britain in the early days of gold and silver coinage, when people would deposit their coins with goldsmiths for safekeeping. The goldsmith issued a certificate with which the depositor could redeem his gold at a later date. These early bankers soon noticed that their certificates of deposit were being used as a method of payment. Why make a trip to the goldsmith when market stallholders were happy to accept a piece of paper as payment?

The goldsmiths then realized that, as long as they kept enough gold coin in reserve to cover the demand for ‘cash’, they could lend out the rest at interest. Some of this loaned out gold would be deposited with other goldsmiths, who would do the same thing. In time they began issuing loans in the form of paper money. It’s not difficult to see how, from a fixed monetary base of, say, 1,000 gold coins, the quantity of money in circulation, or bits of paper that people are willing to accept as money, can rise dramatically. If goldsmiths estimated that they should keep a ratio of ten per cent deposits to loans, then the money supply would quickly grow ten-fold, to the equivalent of 10,000 gold coins, assuming they could find borrowers willing to take up the loans.

This is precisely how fractional reserve banking works today. There is an amount of base currency in the form of notes and coin which is issued by the central bank on behalf of the government. It typically comprises around three per cent of the money supply. Opponents of fiat money dislike the idea of governments having the power to influence the money supply, but under fractional reserve banking the problem is not governments adding to the monetary base, it’s the far greater increase in money supply that occurs when commercial banks make loans to their customers.

‘Fractional’ refers to the fact that banks are (or were until recently) obliged to keep a fraction of their total deposits as cash, so they can always meet the demands of their customers for withdrawals. This also places a limit on the amount they can lend, ensuring that the amount of money in circulation does not spiral out of control.

If properly regulated, these liquidity requirements enable the system to work reasonably well, but over the last three decades they have been steadily eroded to the point where there is essentially no limit on the amount of money that banks can create. Reserve requirements have effectively disappeared. We now have a situation in which, as Steve Keen says, “the banks create as much new money as they can get away with, because, fundamentally, banks profit by creating debt.”

This brings us to the crux of the matter: the principal factor determining the quantity of money in circulation is the banks’ ability to make profits out of the interest they earn on loan repayments. It is therefore to their huge advantage to expand the money supply as much as possible. Over the last three decades, banks have been among the most profitable of all businesses. Their senior staff have awarded themselves bonuses out of all proportion with the ability of the banking system to create genuine wealth. And their shareholders have done pretty well too.

Few people have any idea of the role of banks in creating money. As former derivatives trader Tarek El Diwany says, “The fact is most people think that what a bank does is lend you money that someone else has put in the bank previously. But what a commercial bank actually does is to create money from nothing, and then lend it to you at interest. If I do that, if I manufacture money in my own home, it’s called counterfeiting; if an accountant creates money out of nothing in the company accounts, it’s called cooking the books; but if a bank does it, it is perfectly legal. And so long as you allow fraud to be legalized then all kinds of problems are going to crop up in the economic system that you can’t do anything about.”

Allowing the banks to manage the money supply is the principal cause of both the failure of the economy to promote economic justice, and its inability to avoid the damaging cycle of boom and bust. Since the goldsmiths’ time things have got immeasurably worse. Technological advances mean that most money now exists only as numbers in computers, so commercial banks can create money, and generate profits, at the touch of a button.

The amount of money in circulation is determined by the rate at which banks issue new loans, in which process new money is created. The main source of banks’ profits is the interest received on debt repayments, which further increases the money supply. Supporters of current arrangements argue that banks are simply responding to market demand for credit, and, as markets are supposed always to return to equilibrium, the quantity of money in circulation is always correct. But what banks do is quite different from the activities of other types of firm. They don’t produce any wealth themselves; they support wealth creation only by supervising the monetary system. When that process of monetary supervision itself becomes subject to market forces and the demands of profit-hungry shareholders, there are clear consequences for the real economy. As Steve Keen argues, “firms and banks must be clearly distinguished in any model of capitalism”. Needless to say, under neo-classical economics they are not.

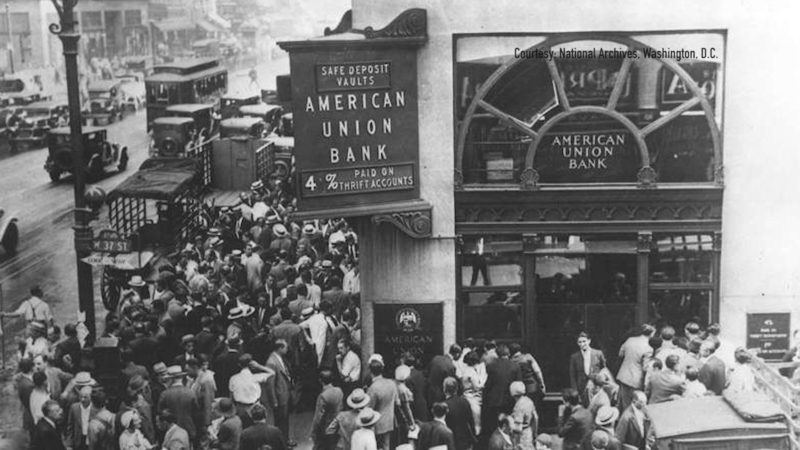

The gold standard failed to prevent the massive credit expansion that drove the stock market bubble and led to the Wall Street Crash. A system of fiat money with barely regulated fractional reserve banking makes it even harder to ensure a stable money supply. History shows that, on the few occasions that money supply stability has been achieved, it has been as a result of properly enforced regulation and close supervision of the banking system. But it’s not just a problem of too much money being created, it also matters what this newly created money is used for.

Excerpt from Four Horsemen: The Survival Manual.

Could this be the year that sends the silver price to the moon and gives the so-called silver stackers their long awaited moment in the sun?

The Great Reset agenda seems to be losing steam and those in charge of implementing it are losing conviction.

The Corona pandemic has exposed the glaring fault lines of some of the world's most clunky and inefficient banking systems.