I recently wrote an article for Renegade Inc pointing out that people in minimum wage jobs today in America, Australia and the UK are doing much worse, relative to the well-off, than they were 50 years ago. The article argues for an increase in the minimum wage in each country, to restore to the low paid their fair share of national income, combined with an employment guarantee at that wage.

One of our readers wrote in, asking us to explain why minimum wage rates have been allowed to stagnate.

I can’t answer this question fully within a few hundred words. If you want a very full answer, and have some background in economics, I invite you to track down the electronic version of my thesis in the Flinders University library. Otherwise, the soon-to-be-published book of Claire Connelly, Renegade’s own editor-in-chief, is recommended. But in the meantime, here are a few hints:

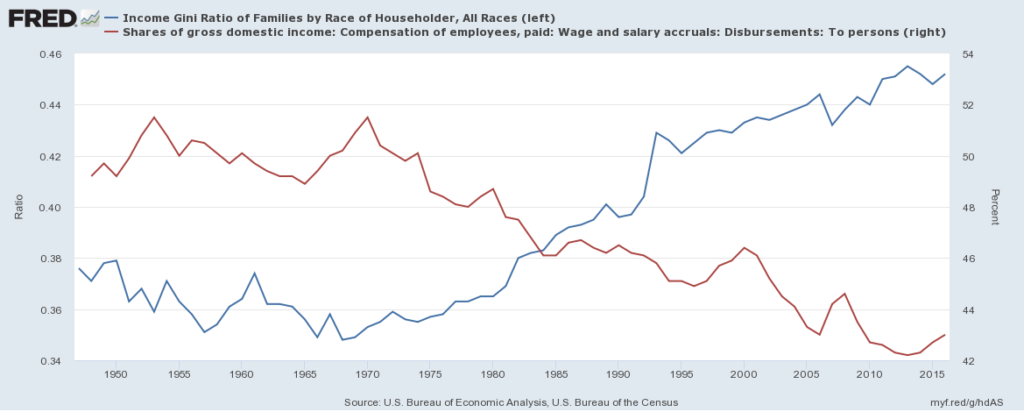

Firstly, it isn’t just about minimum wage rates, and I don’t want to raise the minimum wage just for its own sake. It is about the whole distribution of income. Within most, but by no means all, high income countries, the distribution of after-tax income has become far less even since the 1970s. The US is just an extreme case of this phenomenon.

There are so many other ways in which I could demonstrate the same thing. The rewards of economic growth have increasingly gone to those at the very top of the pile, and increasingly in the form of capital income. Those bang in the middle of the distribution in the US, for example, haven’t done all that well, and the share of labour income in national income has fallen inexorably. It is obvious.

How has this been allowed to happen? It has been in part a consequence of a deliberate plan, but also in part just an evolutionary development.

That it has been partly deliberate is shameful: that is has been partly just the way economies have evolved, does not mean it cannot be reversed.

An increase in the minimum wage is just one of the mechanisms for reversing extreme inequality. Changes in tax systems are another. The reversal of various forms of financialisation are a third. Technology has played a role, but it isn’t the whole story. Globalisation has played a role, but it isn’t the whole story. The power of the already rich to influence political processes and government policies, and the media and public opinion, has been a big part of it, but it isn’t the whole story.

The deplorable failure which is modern orthodox macroeconomics has played a major role.

Worst of all, the total surrender of the political Left, nearly everywhere, in the 1970s, and the utter failure of so-called progressives to stand-up for the ideals on which their parties were founded over the last forty years, led to a long series of neoliberal triumphs, of which the abandonment of those on minimum wage rates was just a small part.

This has fulfilled the wildest dreams of those who formed the Mont Pelerin Society in 1947, with the aim of rolling back the progress of equality and social equity which was emerging from the ruins of War. Its members have accounted for at least eight Nobel prizes in economics since 1969, founded numerous well-funded think-tanks and research institutes, and made major contributions to the partial transformation of the discipline of economics into a tool for misleading the masses, intimidating politicians, and the promoting inequality and privilege.

I say ‘partial’ because there have always been at least some economists like Hyman Minsky, Paul Davidson, Renegade contributors Professors Steve Keen, Michael Hudson, Bill Mitchell and Stephanie Kelton, who have explained how those who were inspired by Milton Friedman and his colleagues have misled the world; how there is a better, more realistic approach to understanding economic systems, which suggests a very different set of economic policies; and how these policies are far more consistent with the principles of which the major left-wing political parties were founded, more than a century ago.

A Friedman neoliberal would oppose any minimum wage, on the basis that it would inevitably cause unemployment. A Friedman neoliberal would advocate for drastic cuts in marginal tax rates on the wealthy, on the grounds that such tax cuts would provide an incentive for investment and risk taking. A Friedman neoliberal would argue for reductions in employment protection, to ensure employers were not deterred from hiring workers in the first place. A Friedman neoliberal would ignore income distribution and would punish the unemployed, on the basis that income depends on productivity, and the unemployed need an incentive to work.

Milton Friedman received a Nobel prize in economics. He was also an incompetent economist, There is no credible evidence that any of the recommendations in the previous paragraph are true. Of course, you could set a minimum wage rate too high, and of course taxes can discourage activities under some circumstances. But the neoliberal project of Friedman and his fellow members of the Mont Pelerin gang, when evaluated in terms the gang themselves would have accepted as a test, has been a failure. Their ideas have been pursued in most places most of the time since the 1970s. Economic growth has not increased, over 1950s and 1960s levels. It has fallen.

What has increased is inequality, social immobility, relative (and in the case of the US absolute) poverty, household indebtedness, financial fragility, and a series of indicators of creeping social failure, one of which is the election of President Donald J. Trump.

Why have minimum wages stagnated? Ideology, ignorance, selfishness, delusion and intellectual fraud.

Call it neoliberalism if you must. But it isn’t just about minimum wages.

What can you do about it? Insist on the reversal of much of the misleading political economic agenda of the last two generations.

What can members of my profession do about it? We have to overthrow orthodox, neoclassical, general equilibrium macroeconomics, and replace it with a better guide for policymakers. What should be in such a new economics? You’ll need to look up the thesis I mentioned above for more on that issue.

Dr Steven Hail

Dr Hail holds a BSc and an MSc from the London School of Economics, in addition to a PhD from Flinders University.

How do you spend your days?

I spend my weekdays teaching financial economics at the University of Adelaide, and my weekends mostly in the Adelaide Hills.

Why is economics important to you?

Economics is important because in the end economists, for good or ill, rule the world. At the moment, it is largely for ill, because the economics profession has become increasingly dominated by the ideas of economists who misunderstand and misrepresent how the economy works, and even what governs human and social well-being. To make genuine progress towards building sustainable and equitable societies, we have to take economics back these people. This is vitally important. As Keynes' says, at the very end of his 'General Theory', "the ideas of economists and philosophers, both when they are right and when they are wrong, are more powerful than is commonly understood. Indeed the world is ruled by little else. Practical men, who believe themselves to be quite exempt from intellectual influences, are usually the slaves of some defunct economist". And as Hyman Minsky said, in 1986 in his great work, 'Stabilising an Unstable Economy', "The game of policy making is rigged; the theory used determines the questions that are asked and the options that are presented. The prince is constrained by the theory of his intellectuals." The defunct economists are in control of the options presented to policy-makers at the moment, and there are a series of questions that are not being asked and options that are not being presented to policy makers, because they are listening to defunct economists, and are not even aware that there is another better way of thinking about the economy.

What drove you to focus on economics. Was there a particular moment you can remember that led you to this field?

As an adolescent, I wanted to understand the reasons for the rise of Thatcherism, and the causes and likely consequences of the changes going on around me in the UK. I think the election of the Thatcher Government in 1979 was the single biggest motivating factor for me to study economics.

What drives you professionally?

I enjoy my job. I don’t need anything to drive me, beyond that. I am a teaching specialist, and my job is to share an understanding of realistic macroeconomics and finance with as many students as possible.

In your opinion what are the three biggest problems facing the developed and developing world?

(1)Climate change (obviously)

(2) The fact that most of the economics profession, almost all politicians, almost all journalists, and almost the whole of the engaged public completely misunderstand macroeconomics, leading to unnecessary underemployment and relative poverty, excessive private debt and frequent financial crises.

(3) The prospect of further wars and terrorism, encouraged in part by the consequences of (2) and increasingly also by the consequences of (1)

If you hadn’t become an economist, what would you have done?

Been a maths teacher.

What led us to this moment in history?

The persistent and successful promotion and pursuit by the Right of a particular way of organising the economy and society, starting in the 1950s, but with sustained success only since about 1980. The craven submission and surrender of the establishment Left, which has more or less en masse accepted the disastrously misleading frame used by the Right for generating and evaluating policy proposals. The tame co-operation of journalists and other commentators in what has now been a long period in which the public have been gradually brainwashed into thinking there is no alternative to what has become known as neoliberalism.

What are the lessons we failed to learn during and since the 2008 crisis?

Fiscal policy works. Governments that issue their own currencies can’t become insolvent in those currencies. Monetary policy doesn’t work, Economies relying on private debt and bubbles in property and/or share prices to grow demand and pursue full employment will eventually face a severe recession. The approach used to manage economies since the early 1980s eventually created a very fragile financial system, and won’t work any more. There will be no return to the pre-2008 ‘normal’ times.

Can you list some ‘Baby Steps’ out of the current economic mess?

Stop talking about a ‘return to surplus’, and shift your concern away from government debt (which isn’t really debt in the conventional sense at all) and towards household debt. Start regulating banks and financial markets properly. Introduce a job guarantee, along the lines suggested by people like Bill Mitchell, at the University of Newcastle in NSW, and Pavlina Tcherneva, at the Levy Institute in New York.

If you were a global President what would your first three pieces of policy be?

To dissolve the world government, as it won’t work. That is the last thing we need. Then I would not be global President any longer, so there would be no need for two further pieces of policy.

Tell us something you have been wrong about?

Spoiled for choice. I used to be, until 10-15 years ago, a largely uncritical teacher of neoclassical (neoliberal) economics. I had started off as an idealist, but (like so many students down the decades) was brainwashed by the single school of thought presented to me, while at university. It took years for me to realise there is more than one school of thought regarding the way capitalist economies work, and that the modern orthodox neoclassical way of looking at the world has rotten foundations and is in many ways disastrously misleading. I try to be compassionate to those still thinking within a neoclassical frame, because for a long while I was one of them, and I know how very hard it is to escape that frame. In some words of Keynes, written in December 1935, ‘the difficulty lies, not in the new ideas, but in escaping from the old ones, which ramify, for those brought up as most of us have been, into every corner of our minds.’

You are stuck in a ski lift for twenty four hours - you can have one person (living or dead) with you who will it be?

My late mother. Sorry – not interesting, but true. If forced to pick someone else, it would be John Maynard Keynes. Predictable perhaps, but it would. (1) Mum (2) JMK. Perhaps I could have them both there. We’d have a great time of it.

Name the book that changed you….

On Being a Christian, by Hans Kung.

This is the book which finally convinced me I was (and am) an atheist.

What would you do differently if you were to start all over again?

Move to Adelaide sooner. I left London in the year 2000. Wish I’d come here in about 1990.

Give our readers, members and subscribers a piece of advice that has served you well… Anything you would like to plug? Now is your chance.

The best piece of advice I have ever received is to have limited expectations about changing the world for the better, but to keep trying anyway. I have never voted for the winning side in a general election in the UK or Australia. It would be easy to be discouraged. But it is important to me to retain a sense of purpose, and even if making genuine progress is a very long game, to at least do my best to be helpful, and to not be remembered as a flat-earther (which is how many of today’s most prominent orthodox economists will be remembered in the decades to come).

I encourage everyone to take an interest in modern monetary theory. An easy way of doing this is to watch the many presentations by and interviews given by Bill Mitchell, Stephanie Kelton, Warren Mosler and Randall Wray.

Latest posts by Dr Steven Hail (see all)

- Why have wages been allowed to stagnate? - January 4, 2018

- A just social-wage and a job guarantee - December 28, 2017

- Household Debt: A Tale of Three Countries - July 18, 2017

We are just now going through this in Ontario Canada where the government is raising the minimum wage. There is the usual squealing from employers and neoliberal talking heads. Unfortunately workers, employers and government are all looking at it through very narrow lenses. For example, small business does have a valid point but no one is looking at helping them to afford to pay decent wages by reducing their deadweight costs through the types of tax-shifting measures often recommended on this site. Also very few people point out that wages are the main source of demand - if you pay people they have something to spend! We have pretty much exhausted government income transfers and consumer borrowing as (fake) demand creators and need to go back to basic principles.