Neoliberalism does not do what it says on the can, and Economist Dr Steven Hail has the charts to prove it.

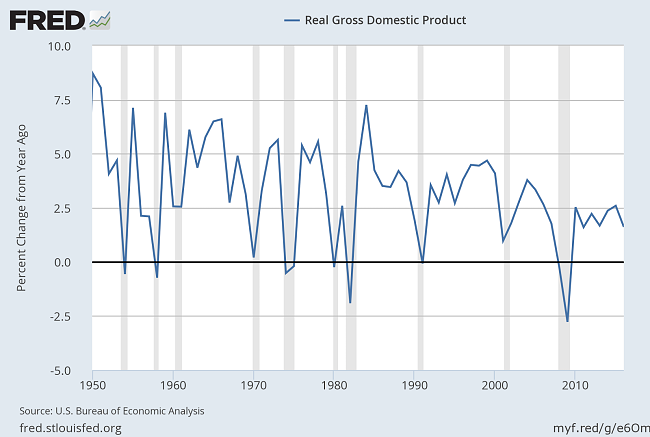

During the 1950s and 60s, the US economy grew at an average annual rate of 4.4%; in the 1970s and 80s, at an average rate of 3.2% per annum; in the 1990s and 2000s, on average by 2.5% per year; and since 2010 it has growth by about 2.2% each calendar year.

Now economic growth should not be the be all and end all of economic policy, for sure. Growth which continues to destroy our eco-system is not something we can afford in the future. Moreover, other issues like income and wealth inequality which could possibly, under some circumstances, conflict with the objective of higher growth are important. This is particularly so, given the evidence that increases in income, beyond a certain point, don’t appear to add much to our sense of subjective well-being, and that by a variety of metrics, successful societies have been shown by social researchers to be more equal and more equitable ones, rather than necessarily those with the highest incomes.

And yet, we have put up with orthodox economists for generations now, drumming into our heads the following messages:

- Maximising economic growth is the over-riding objective of policy.

- Reducing the higher personal tax rates and making the tax system less progressive sharpens incentives for investment and risk taking and raises productivity growth.

- Budget surpluses, or at least balanced budgets, promote economic stability and growth.

- A deregulated and bigger financial system promotes economic efficiency and growth.

- The best way to promote social well-being is to cut top tax rates, deregulate, financialise, and allow those at the bottom to benefit from the higher growth via a trickle down effect.

By their own metrics, the orthodox economists appear to have failed in the USA. The promises they made back in the 1970s and 80s have not been met.

Perhaps it is easier to see this using a graph. Here you go, US economic growth since 1950. It’s not going up, up, up, is it? Don’t forget that this might not be your or my objective, but it was the objective of the people who took over economics a generation or two ago.

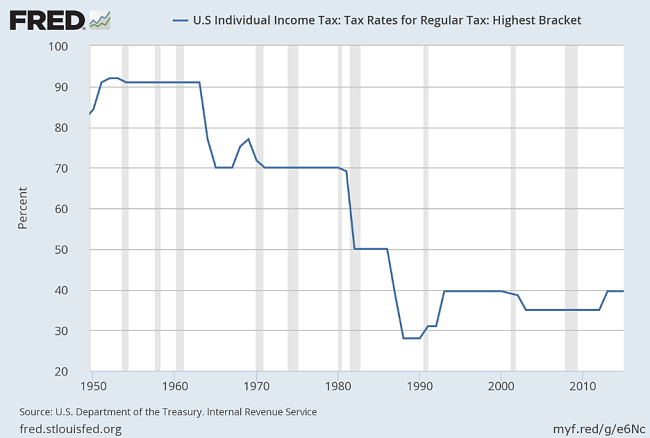

Now let’s take a quick, and so not very scientific, but honest look at the top marginal rates of income tax in the US. I don’t need to give you any figures this time – the chart speaks for itself. Look at the top tax rate in the 50s under Eisenhower, or the 60s and 70s under Nixon. Commies! They make Bernie Sanders look like Milton Friedman. They make Jeremy Corbyn seem positively Thatcherite, by comparison:

It is interesting, isn’t it, that the cuts in the top personal tax rates have been combined not with an acceleration of enterprise and growth, but with the precise opposite. The results have been the opposite of the stated objectives.

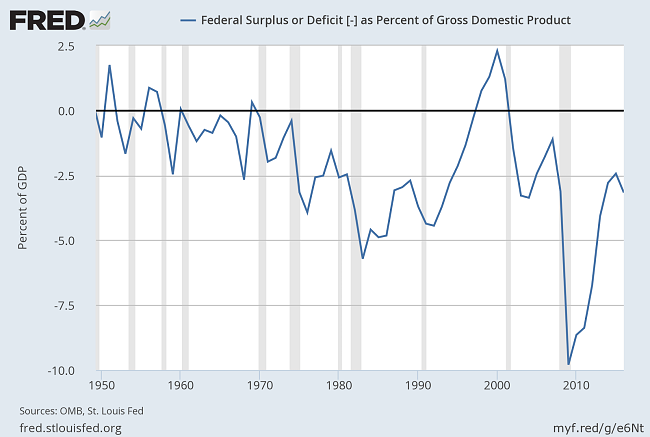

What can we say about the fiscal balance – budget deficits and surpluses?

The first thing to say is that the US government, like virtually all other governments, does not, has not and will not in the future ‘balance the budget’ or run surpluses over time. A balanced budget law would be economic suicide. The US government ran (tiny) surpluses very briefly twice in the 50s and again in the 60s, each time being followed by economic downturns, as you can see in the earlier chart. The only other ‘surplus’ was the Clinton one, which Bill and Hillary and their friends still like to boast about, but which was combined with an unprecedented build up in household debt, and bubbles which burst in both the stock market and then (catastrophically) in the housing market.

The lesson from history, and from basic national income accounting, is that if the private sector overall wishes to add to its savings and if the rest of the world wishes to acquire US dollars (this became strongly the case after the year 2000, as China and others decided to accumulate large amounts of US dollar reserves) then a fiscal deficit will be necessary if the economy is to remain anywhere close to full employment, without a private debt fuelled bubble taking place. The fiscal deficit after the year 2000 was not large enough to offset the growing trade surpluses of countries like China with the US, on which those countries were basing their growth strategies, setting the stage for a crisis.

Remember, the US government cannot ever run out of US dollars, unless it chooses to do so. It is the currency issuer. They can and almost certainly will run budget deficits nearly all the time for ever (or until there is no longer such a thing as the US government).

What about social well-being? The US has always had a relatively high level of inequality, but as many people have pointed out in recent years, the changes which have taken place there since the 1970s have taken this to a new level, or rather back to an old pre-1930s level. We are back in the Great Gastby, 1925, Scott Fitzgerald, and all that. You want to know where Donald Trump came from? Screwing down ordinary Americans, while brainwashing them with lies about a land of opportunity, and berating any complaints as being born out of jealousy, or what we Aussies call the tall poppy syndrome, or worse still, and horror above all horrors, socialism!

Remember, the US government cannot ever run out of US dollars, unless it chooses to do so.

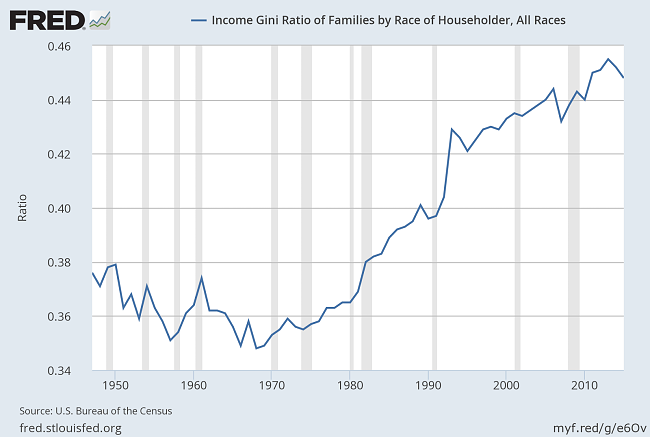

The Gini coefficient is a measure of inequality which lies between 0 and 1, where higher values indicate more inequality. You don’t need to know the details to understand what this chart is telling you (and bear in mind this is for income and not wealth, where the data would be even clearer):

Inequality was continuing to fall somewhat, in the golden years up to about 1970, since when it has skyrocketed so that the US now has income inequality typical of a third world country, and not of a civilised and successful society. We are back in the belle epoque for the rich. Pass the champagne, Donald!

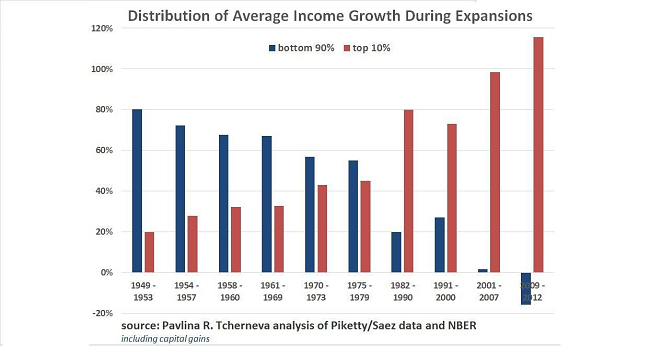

The economist Pavlina Tcherneva has produced the following highly informative chart, which can be accessed on her web page:

What it shows you is that until the 1970s most of the income growth during periods of economic expansion went to the bottom 90% of the population: since then, most has gone to the top 10%, and increasing the top 1%. During the period from 2009-12, under the champion of the elite Barack Obama, so much went to the top 10% that the bottom 90% actually went backwards. The economy was growing, unemployment was falling, but people’s incomes were actually falling. Not much trickle down there!

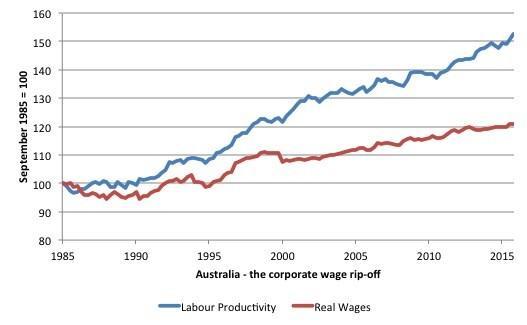

Hardly any of the very substantial growth in US labour productivity since the early 1970s has gone to workers in real wages, and consequently nearly all of it has been delivered to capitalists and investors. It is important to emphasise at this point that this is not a purely US phenomenon. These trends have developed later in countries like Australia, than in the US, and in most cases have not gone so far, but we can see a similar story in the Australian data, reproduced in this chart from the blog site of Professor William Mitchell of the University of Newcastle, NSW:

And how did that deregulated financial system go? The economist Hyman Minsky, a long time ago, explained that a deregulated financial system would tend to take on more and more risk during times of relative economic stability, and consequently become increasingly fragile, leading to more frequent and more severe financial crises and to eventually a Great Recession. He classified economic management which did not take this tendency into account as ‘inept’. It seems the US and the rest of the world wandered ineptly towards the Global Financial Crisis of the last decade, at least in part through ignoring economists like Hyman Minsky and choosing instead the economics of Milton Friedman and the neoliberal right.

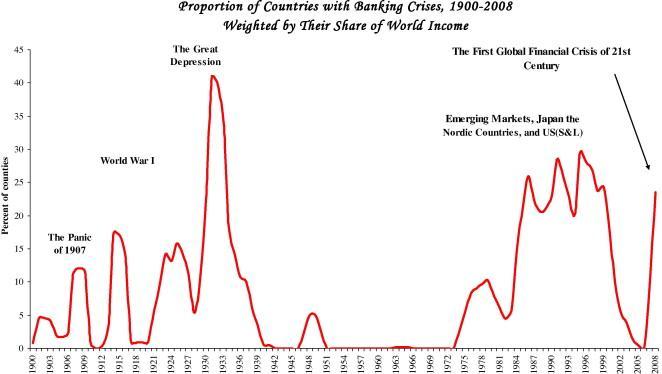

One more chart might be helpful. This is taken from a 2013 paper of two leading orthodox economists, who are hardly radicals, Carmen Reinhart and Kenneth Rogoff:

The 1950s and 60s are a unique period in global economic history. A period of economic growth, falling inequality in many countries, rising living standards, and virtually nothing which could be described as a banking or financial crisis. And yet, even by the late 60s, Minsky and a few others started to warn of a drift towards fragility and a loosening of the regulations which had allowed this unparalleled period of financial stability to exist. By the end of the century, almost the the whole of the regulatory framework put in place during and after the Great Depression to stop ‘It’ happening again had been dismantled.

Hardly any of the very substantial growth in US labour productivity since the early 1970s has gone to workers in real wages, and consequently nearly all of it has been delivered to capitalists and investors.

What’s more, policy makers, sometimes deliberately and sometimes because they don’t dare face the truth, have in most cases not yet taken in, or taken seriously, any of the above.

Sure, growth for the sake of growth is not what we should aim for – it is indeed ‘the ideology of the cancer cell’, to use the words of Edward Abbey. But there is no evidence that less progressive taxes have promoted growth anyway. There is no evidence that more inequality has contributed towards growth. There is no evidence that deregulation has contributed to growth or to stability or social well-being. There is no credible evidence that trickle-down economics works. None whatsoever. It is a fallacy. An article of faith, perhaps – but not of science.

Almost everything which almost all policy makers have taken for granted and asked us to take for granted for more than a generation has been proved wrong. We were closer to the truth, it seems, in the 1950s and 60s, and there must be some lessons for us there.

Economists like Mitchell and Tcherneva, whose charts I have reproduced, and other modern monetary theorists, and politicians like Bernie Sanders and Jeremy Corbyn, have had some success in bringing the above to wider public attention. They don’t advocate a return to the economics of the 1960s, but they and other do advocate an abandonment of the economics and politics of neoliberalism (and of ‘New Labour’ and the ‘Clinton Democrats’), and a shift to a modern progressive, inclusive, equitable approach to economic policy and political decision making.

With workers pushed to breaking point, is it now time to call time on predatory business models?

Both COVID-19 and the climate crisis are being used as camouflage for central bankers to throw more printed money into a broken system.

With proper access to land denied to the vast majority, is it now time to reclassify trespass as a revolutionary act?