Treating federal budgets like that of a household has starved economies of precious resources, destroyed productivity, put downward pressure on wages and has facilitated unprecedented levels of private and household debt. Claire Connelly explores the consequence of this logical fallacy in an excerpt of her upcoming book, How The World Really Doesn’t Work.

One of the classic fallacies of logic is to believe that what works for one person, will naturally work for everybody, and that therefore surely all of us can do the same thing at the same time and expect a beneficial outcome.

In economics, this is highly unlikely to be true.

‘If everybody tried to sell GM stock at the same time for example, probably really, really bad things are going to happen to the GM stock,” says economist Professor William Black.

Black is an American lawyer, former bank regulator and Associate Professor of Economics and Law at the University of Missouri-Kansas City.

“It’s going to get pushed downwards, essentially to zero,” he said.

But all of the people who bought that stock still have to pay back the loan. This is what is known as ‘Buying on Margin’ and can lead to severe liquidity crises to boot.

Likewise, when a government analogises its budget to that of a household, bad, bad things happen. It is this very logic of composition that contributed to this terrifying moment in history.

The bid to balance the budget has sucked trillions of dollars out of the economy, destroyed productivity, put downward pressure on wages and employment, encouraged unprecedented levels of private and household debt and has encouraged financial deregulation which has led to inflated property, equity and auto-loan bubbles in a desperate bid to keep the economy afloat.

Contrary to popular opinion, government spending does not leave a debt that future generations must repay, at least not if you use your own currency and are not on a gold standard.

Contrary to popular opinion, government spending does not leave a debt that future generations must repay

This is because a government budget is not the same as a household budget.

A household does not print or issue its own currency. When funds are running low & rent or mortgage payments are coming up, we can’t just put in a phone call to our mates at the RBH (Royal Bank of Households - not a real thing) and tell them to issue more money.

But the government can. And does. In fact every time the government spends on public services, it does so by pumping newly created dollars into the economy.

Whether a government can run out of money depends on what kind of government it is, and what kind of money it issues.

A Federal Government that issues its own currency (what is known as ‘sovereign currency’), only borrows in its own sovereign currency and a floating exchange cannot run out of money.

Only the US Federal Government can issue American Dollars. Only the Australian Government can issue Australian dollars. Only the UK Government can issues pounds.

These are what are known as ‘sovereign currencies’. A sovereign currency is a currency issued by a Federal Government, with the power to create and issue its own legal tender, which it spends into circulation, and then takes back from the private sector in the form of taxes and other compulsory payments to itself.

If you or I tried to print US dollars, or Australian dollars or pounds we would be counterfeiting. If the US government began issuing Australian dollars, it too would be counterfeiting.

A central bank usually controls the supply of money and sets interest rates. Every time the Federal Government spends, it creates money. It does so by crediting the reserves of commercial bank accounts held at the central bank. (In the US, this is The Federal Reserve, known colloquially as The Fed. In Australia it is the Reserve Bank of Australia, in the UK the Bank of England, and so on). The commercial banks in question then credit the bank account of whoever is the beneficiary of that spending. For example: state and local governments or councils and the services they administer: Police, Hospitals, Fire etc.

It does this with the assistance of the central bank, which does not control any measure of the supply of money in the economy, but instead controls the rate of interest at which commercial banks can obtain additional reserves when they need them.

State and local governments can run out of money because although their budgets are often largely financed by federal spending, it is the Federal government which limits that funding. State and local taxes, and borrowing by state and local governments are then applied to make up any shortfalls. So if a state government raises its spending without an increase in its funding from the Federal government, it must also raise state taxes, or issue debt, which it will later need to repay. It is not a currency issuer. The Federal Government is in a very different position.

Of course, a federal government can also choose to run out of money by forbidding itself to make any: for example the US debt ceiling. The imposition of this ceiling in the US was originally a political gesture, 100 years ago, and has no economic justification or motivation. It has always been lifted, down the years, when reached, and could be scrapped by Congress at any time. So-called debt ceilings are not to be found in most other monetary sovereigns. They are artificial limits.

“You can simply say you cannot have more money, in which case you would be putting artificial limit on yourself,” says Professor Black.

People can choose to default. Russia, for example, chose to default in 1998, even though it had a sovereign currency. (This is the only default on monetary sovereign government debt in modern times). Periodically Republicans in the US context have tried to make us default, by refusing to pass the debt ceiling, even though the debt is going to go above the ceiling.

“If they succeeded long enough the US Government would have defaulted on its debt. It would be the stupidest thing in the western world, but it could be done.”

Professor Black likens the US debt ceiling to the infamous scene in cult film Blazing Saddles where the newly appointed black sheriff in a confederate town avoids a lynching by threatening to shoot himself in the head:

“The whole idea of that being funny is that it is nuts,” says Professor Black. “But that is actually what they try to do with the debt ceiling. Ok, we’ll shoot the US economy in the head.”

Countries that do not have sovereign currencies can run out of money, because they are essentially borrowing in foreign currency. In this context, it makes sense to have a debt ceiling.

“A debt ceiling makes sense if you don’t have sovereign currencies,” says Professor Black. “Then you can default. You can get in lots and lots of trouble if you behave like you have a sovereign currency when you don’t.”

Countries that could potentially run out of money include Argentina, some of the smaller countries which use the Euro including Greece, Cyprus, Malta, Slovakia, Estonia, Latvia and Lithuania. Probably less likely if you’re France, Italy, Spain, Austria, Portugal, Finland or the Republic of Ireland but it’s not impossible. Any government with obligations in a foreign currency, or in a currency it does not issue, can run out of that currency.

The lesson is to keep your own currency, have a floating exchange rate, and not borrow in foreign currency.

Governments which issue currency, which only borrow in that currency and allow those currencies to float, cannot run out of money. Indeed, in a sense they are not borrowing at all. How can you meaningfully borrow something you create and which in principle you could create at zero cost and without limit?

“You can’t run out of money unless you run out of electronics,” says Professor Black.

Countries with sovereign currencies include America, Australia’ the UK, New Zealand, China, Canada, and Japan. Argentina for a while had a sovereign currency, but effectively gave away that sovereignty by its actions.

Countries that cannot run out of money include America, Australia, New Zealand, The UK, Canada, China and Japan

Of course, it is possible to take seemingly sovereign currencies and make them behave as though they are not sovereign and is generally not a good idea, as Argentina recently found out.

Onwards…

Economist and co-founder of LF Economics, Philip Soos says America is just as vulnerable to another financial crisis as the UK and Australia and Canada.

“It’s not great when people are massively leveraged up to the eyeballs in housing and have very little actual savings,” he said. “A lot of their financial wealth is created by investments in equities and superannuation, and is exposed to housing and the banks. It’s not great and you can see why so many governments are desperate to avoid any downturn in housing as its effects rebound throughout the economy.

The US central bank, The Fed recently increased interest rates, but what differed between this time and every other period in post-war history, is that the Fed is raising rates into weakness,” Soos says.

the Fed is raising rates into weakness

“Whereas all other previous rate rises have occurred in a strengthening economy.”

In the US the unemployment rate has come down but wage growth is anaemic. American consumers are heavily indebted. Mortgage and household-debt rates are picking up as property prices inflate.

“There is a massive equities bubble, a huge student loan bubble, and a massive auto loan bubble,” says Soos.

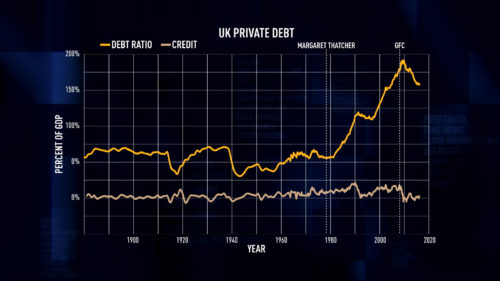

The UK has been crippled by austerity. Data from the British Office of National Statistics shows that non-government saving ratio has plunged, household debt has escalated sharply, non-mortgage debt has accelerated and for the first time since the 1970s, real household disposable income growth has been negative for three successive quarters.

Obsessed with fiscal surpluses, Canada officially went into recession in 2016, following two quarters of negative growth and a resources boom that came to an abrupt halt. Like Australia, Canada has a property bubble which is fit to burst, escalating private debt, rising unemployment and declining growth.

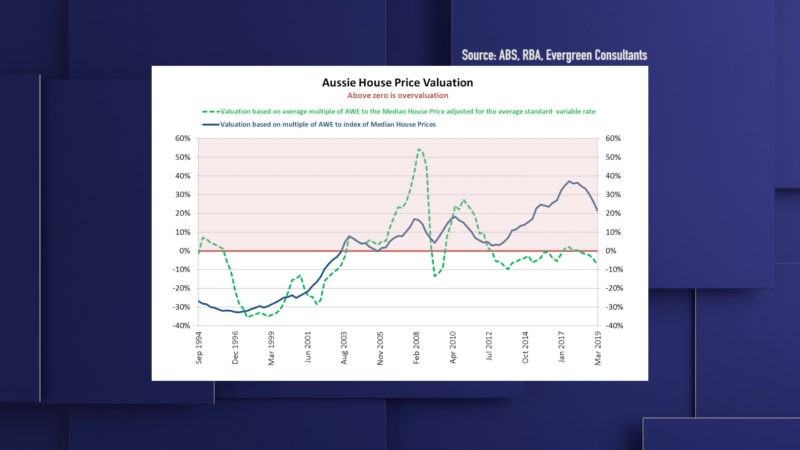

Australia officially went into recession in May following two quarters of negative growth. Our GDP hasn’t cracked 3% since 2013 and has only risen above that level four times in the last nine years. Australia’s wage growth is stuck at record lows and its household debt to GDP ratio hit 123% in February.

“There is a massive equities bubble, student loan bubble, and a massive auto loan bubble,” Soos says.

There is a massive equities bubble, student loan bubble, and a massive auto loan bubble

“Because the GFC really provided a litmus test for what would governments would do in the face of huge criminality in the banking system, which was to bail out the crooks and protect them, it entrenches moral hazard.”

The state of the global economy is the result of growth without employment, of forcing people to leverage themselves up to the eyeballs in debt in lieu of reliable income.

Central banks cannot continue to cut rates forever, and rates are already negative in Europe and Japan.

Eventually governments will be forced to confront the truth which is that by treating its budgets like that of a household, they have starved their economies of precious resources, creating global insecurity which have contributed even further to rising social and political tensions.

When it comes to what can be done, Soos says rule of Occam’s Razor applies, (where the most obvious answer is almost always the correct one), which is that to avoid another financial crisis, governments must, finally, address the health of their economies: Fix productivity, stimulate employment and reduce household debt.

To avoid another financial crisis, governments must, finally, address the health of their economies: Fix productivity, stimulate employment and reduce household debt.

The New Deal pulled America out of the Great Depression. Job Guarantees across America, the UK and Australia saved their respective countries from ruination following WWII.

At a time when wage-growth is at its lowest point since the end of the war, another job guarantee doesn’t sound like such a bad idea.

“Given the huge stock of household debt, it is more critical than ever that governments ensure full employment, stimulate wage-growth and help bring down the giant stock of private debt and help people make inroads to pay large chunks of it off,” Soos says.

To do this, they will have to change the narrative on government debt and government deficits, and accept that government debt is an essential substitute for household debt and that government deficits support private incomes and allow for private saving.

The question now is whether it will take another crisis for governments to unlearn the lessons they’ve been getting wrong on the economy for the better part of 30 years.

Read a more detailed excerpt of my book by subscribing to Hello Humans, a subscription journalism experiment founded and run by yours truly, starting at just $1 a month.

Most employment law, if not all of it, needs to be thrown out and replaced with legislation that wasn’t built on more than 150 years of master/slave law and precedent.

One of the greatest social problems we face is the virtual debt prison, has the time now come for the masses to break free from the economy's debt vultures?

Government and household budgets briefly explained.