Published: 16 June 2018

Guests: Mitch Feierstein

Further reading: Adults In The Room: My Battle With Europe’s Deep Establishment

Ten years after the great financial crisis, markets are again booming, but as are levels of debt and leverage. Is this a cause for concern or have policymakers fixed the fundamentals? Has complacency led investors to take on greater risks or have they learnt the lessons of 2008? Is Brexit a blip as the Eurozone is actually in rude health? Or are the fault lines increasingly clear but papered over?

As volatility returns to markets, we ask: what lies beneath the global economy?

Stock markets are near all time highs. Bankers are taking big bonuses once again just as America shapes up for the mother of all global trade wars. What could possibly go wrong? If the commentators are to be believed, we are back to business as usual. But if your intuition tells you something different, you might be onto something.

Joining us to work out what is really going on in the markets and the wider global economy, is investor, hedge fund manager and author of Planet Ponzi, Mitch Feierstein.

Feierstein recently tweeted: ‘let’s party like it’s 1929’ and tells Renegade Inc. that the banking sector has pulled off one of the greatest Ponzi schemes in history, which began with the 2007 global financial crisis.

“Have things really improved since then?,” he says. “I mean, none of the banks - as you see the share action in Deutsche Bank, one of the largest banks in the world in terms of derivative positions off balance sheet - should be zero, because their enterprise value, if you look at the liabilities they have and you use real accounting, there is a systemic problem.”

A lot of European banks have not de-leveraged. Italy is in huge strife. Feierstein says the proverbial can has simply been kicked down the road.

“What has happened is central banks, the European Central Bank, the Bank of England, the Bank of Japan and the United States Federal Reserve have printed unlimited quantums of money which have repressed interest rates to historic lows, making credit available and liquidity available to people who shouldn’t have it,” he says. “Creating zombie institutions and zombie banks.”

Zombie institutions are those whose liabilities are much greater than their assets.

“Like probably every bank in Italy,” says Feierstein. “The problem with that is these banks need to be recapitalised. I don’t know any investor that’s going to want to jump in and put their capital at risk.”

The danger is that when liquidity dries up, there’s no meaningful lending that can occur and ultimately the bank falls over.

“What happened last time in 2007, there were a lot of funds and a lot of the banks, what they were doing was lending longer term and borrowing in the short term to cover their long term liability,” Feierstein says. “And when people become concerned about who you’re lending money to they say: ‘oh my God. Maybe these guys aren’t as creditworthy as we think, so we’re going to cut back on lending to them’. Once the lending becomes constricted or restricted, then the counter parties start getting cut off.

“You don’t know at the end of the day who is going to go bust. Somebody might go bust, but there’s a systemic problem. And then all liquidity gets cut back on*.”

Renegade economist and friend of the show, Professor Steve Keen says that the herd behaviour is a fundamental aspect of capitalism that is left out of conventional economic theory.

“Orthodox economists don’t believe in herds,” he tells Renegade Inc. “We believe we’re all individuals and make rational decisions and therefore we don’t have any crisis in the future. The reality is we do have herd behaviour and people will follow the herd and for a while. When you’re following the herd, you can make money when the system is going up. The trouble is any herd crashes over the edge of a cliff at some point.

“It’s the person who is aware of what’s going to happen and doesn’t join the herd when it’s getting close to the cliff, they’re the ones who survive.”

Contrary to herd wisdom, financial crises are not unpredictable, black swan events. In 2005, Professor Keen was one of the few economists in the world who accurately predicted the US housing market crash and the global financial crisis. What was he looking at that mainstream economists ignored?

“The private debt bubble caused the boom beforehand,” he says. “The bursting of that bubble caused the downturn, and that driving, rising level of private debt itself is what caused the increase in stock prices. The crash in the rate of growth of debt is what’s caused the plunge in stock prices. So they think they can create bubbles without using more debt to do it. They can’t.

“Their recipe for getting us out of the crisis is to add to the debt that caused the crisis in the first place.”

Is quantitative easing a tool to buy time or is it there to fix a structural problem? Because when you look across Europe there are clear structural problems.

Feierstein says that quantitative easing (QE) was a temporary buffer but says it relies on Keynesian economic theory where economists think they can create aggregate demand.

He says the theory goes that enough supply creates its own demand.

“But it’s ridiculous because it doesn’t work,” he says. “That will work in limited cases, if you’re in a surplus situation, but we’re not in a surplus. It’s the same thing as I’ve been saying since 2008/9: you can’t pay your way out of debt with borrowed money. If you keep borrowing more money, the only thing that’s happening is you’re accruing more debt that can never be repaid. Which is exactly what Italy is doing.

“Italy owes around $4 trillion dollars now. If you look, there’s 152 countries in the world odd or something. If you look at what happened to Italy since they joined the Euro in 1999 to today, Italy’s like 150 in terms of their gross domestic product.

“There are only two countries that have had worse GDP than Italy and they’re Haiti and Zimbabwe.”

The investor says the single currency has destroyed Italy, and the country’s population is fed up and perceive the Euro as a failed project.

“The Euro, the single currency Euro can never work,” he says. “Nobody, not the southern Europeans, can ever be on par with Germany. And until there’s a central treasury and everybody gives up their sovereignty for the good, for the greater good, it’s just not going to happen.”

So what happens to the market if central banks stop their QE programs?

“I’ve coined a phrase: You can never taper a Ponzi scheme,” he says. “The quantitative easing program is a massive Ponzi scheme.

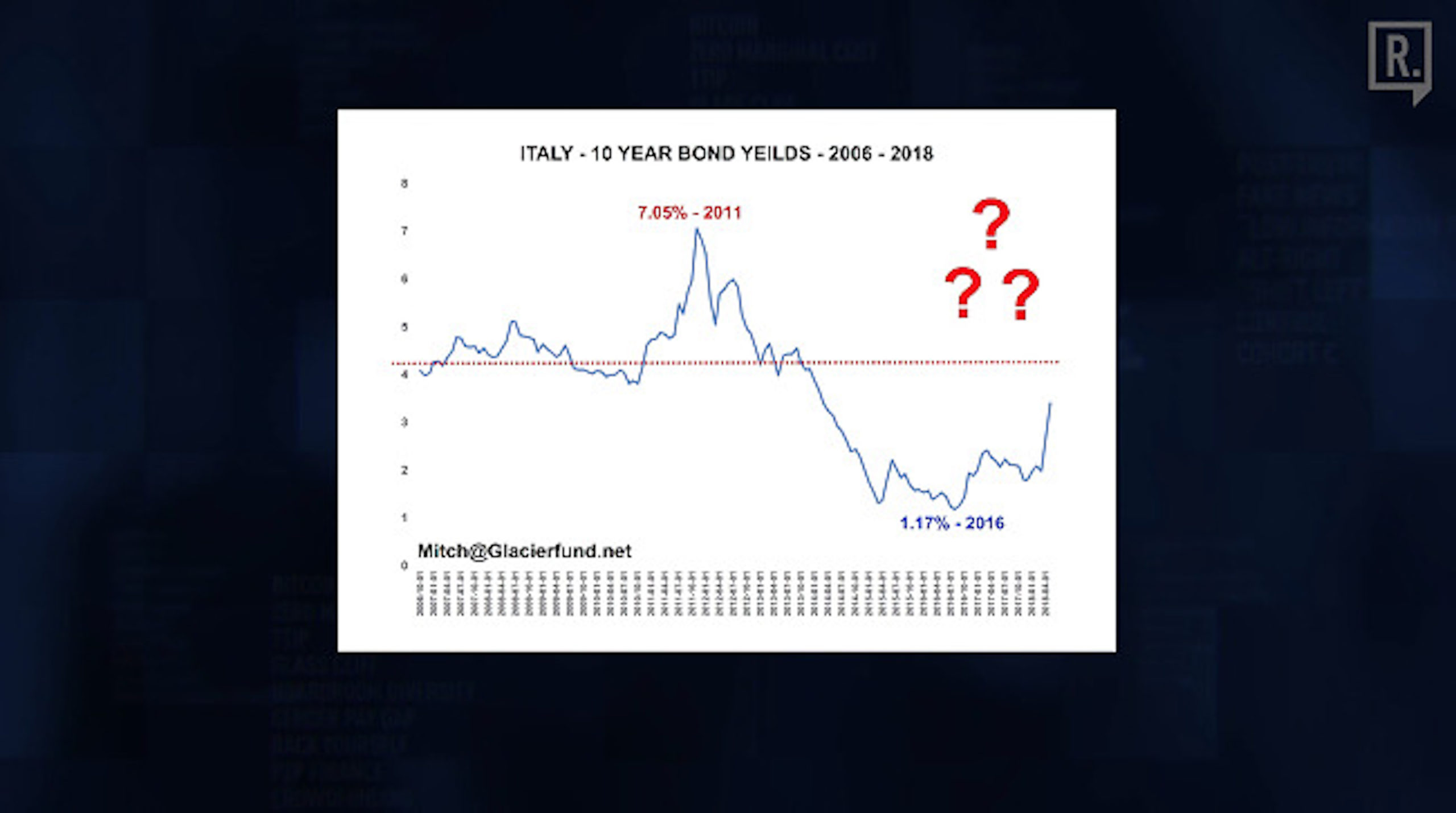

“You’re creating more money. There’s another dummy coming into this scheme to pay back the first dummy. It’s the greater fool theory. So the problem with them trying to taper is, here we have a chart of the Italian bond market, the 10 year bond market:

“If you look back in 2011, we went to 7.05%, and then 2016 the low yield was 1.17%. So that’s tenable. But you can see the dotted red line, when you go above that, where the question marks are, then you reach a point of insolvency, where your revenues will not be equal to the amount of debt service that you have to cover on the existing debt that you have.”

When the Fed claims it’s going to normalise interest rates in the United States that’s an impossibility because mathematically it just doesn’t work, the investor says.

“Central banks are liars, quite frankly,” says Feierstein. “That’s the bottom line.

“If you look at Mark Carney, for example, in the United Kingdom, who created the biggest housing crisis on the planet in Canada, and then George Osborne hired him to come over and do the same thing in the UK. If you look at the number of times in Canada he said he was going to raise rates and he ended up cutting rates. And then when he came to the UK, the first couple bravados he said: ‘I’m going to raise rates, I’m going to raise rates, I’m going to raise rates.’ He’s never really raised rates, and they haven’t cut the amount of money that they’ve been printing here.

“As I’ve always maintained there’s got to be a direct correlation between house prices and affordability and the amount of income generated by the person who has to pay it. It’s not like an ATM where you can just expect £500 to return every day because the prices keep going up, up, up and up. This is the big mistake that was made by all the all the lending companies during the first collapse in 2007/8.”

Feierstein says they have simply repeated that behaviour post 2008, except it’s worse now because there’s more leveraging credit in the system now then there was during the credit crisis.

“We’ve taken up the tops,” he says. “No lessons were learned and it was enabled by the reckless lending by the central banks.”

He describes the situation as sitting in the back of a Rolls Royce Corniche trying to drive through the Sahara Desert. It’s 103 degrees and your driver says: ‘Sir, this red light is blinking. I don’t know what it means by the E signal’, and there is no petrol station in sight for 200 miles: so you’re going to suffocate in the heat.

The fuel is debt. The transaction or the mechanism to bring that into play is the housing or real estate markets, predominantly. All the lights are flashing. How does this end?

“It’s impossible to call what the trigger is,” says Feierstein. “Housing might be a trigger but you’ve got to think about commercial real estate, as well as residential real estate. These are gigantic amounts, quantums of money that have been lent out. There’s also problems in the credit markets because there are companies, like, for example, for the next four years or five years in America there’s $4 trillion in resets that have to be made in investment grade and high yield credit.

“High yield credit, for example, that market, people are lending at ridiculously low levels just to get yield. Like, Argentinian issued an 100-year bond issued in June of 2017. The finance minister announced it at Davos and he said ‘all our problems are solved!’.

“I was like, ‘look, anybody who buys this 100-year bond from Argentina, one of the countries that has defaulted the most in the history of the planet almost, in terms of finance, deserves to lose everything they invest’.”

The bond was oversubscribed by about eight or $12 billion.

“It’s the herd trying to chase yield and the problem of having inexperienced traders who are in their late 20s to mid 30s just chasing yield,” says Feierstein. “It traded above par at one point, and now obviously they’re going to the IMF because they need a bailout. It’s only been 18 months. So the 100-year bond, the idea that anybody would buy that is just insane. But it’s part of the bigger program: The fear of missing out.”

On the QE point. There are traders out there who are looking after pension funds and investments, for people watching this. They have never known anything but QE. Their mantra is: don’t fight the Fed. Because ultimately the Fed’s always going to step in for America, or a bank of England here in the UK or ECB and ultimately saves you. Is it the case that central banks can keep stepping in every time this thing hits the buffers?

“Can the Fed keep coming in? No,” says Feierstein. “Because eventually they are going to run out of bullets. The massive amount of debt that has been accrued has happened in the last seven years. I don’t know what the stumbling block is going to be, but there’s there’s too much liquidity in the system and there’s too much sloshing around. So all the people who have been buying the dip, every trade will always work for a certain amount of time, but you don’t want to be last in on something that’s a runaway train like this.

“You have to take a step back and look and say ‘look, where my exposures and what can I do to mitigate?

“It’s not going to be about return on capital it’s going to be a return of your capital. You’ve got to be proactive. When it collapses, we are going to see a massive collapse. There’s going to be no time to get out.

“So you might have what’s called a ‘lock limit down’, where the markets actually gap down by 1000 points and there’s just no way to get out.

“I think some of the dangers in the past six or seven years are these exchange traded products like the ETF which is a basket filled with different stocks. What can possibly go wrong? These are good instruments when the market goes up, but when everybody wants to sell at the same time, is there going to be enough liquidity? I question whether there’s going to be enough liquidity.

“Now, if you look at the prospectus of these ETFs, it says somewhere on page 380 or 500, in tiny print. If you get out your magnifying glass it’ll say: ‘we can’t guarantee that this ETF will replicate the underlying asset class that we purport that it’s related to’.

“And the kicker: ‘In times of stress we can’t guarantee that you’ll ever be able to sell this and the price may go to zero’. So the risks are always in the prospectuses of these products. Buyer beware: You should read that 500 or 600 pages or not invest in the product.”

Today there are $223 trillion in financial assets, which is three times global GDP. The last time this ratio reached these levels was during the Great Depression. If incomes do not grow, then more debt is the only way to boost spending. This policy of extend and pretend does nothing to fix the underlying problem because the new money does not end up with those most likely to consume. Instead it remains stuck in pools of capital, chasing declining yields.

For as long as this continues the debt ratio and systemic instability will continue to rise. This is known as the Minsky cycle. Only rebalancing through debt forgiveness or default will restore the system. The problem we face is that right up until the cycle’s turning point, the opposite appears true, that things are becoming ever more stable.

Professor Steve Keen tells Renegade Inc. that the conventional way of thinking about finances is that finance is another profit centre in capitalism: you’ve got industrial sector which is profits, service profits, finance profits etc.

“Finance fundamentally is not a profit centre it’s a cost of doing business,” he says. “And if that cost gets too high then you actually weaken the remainder of the economy, you don’t strengthen it.

“So what you get is the risk of capitalism is being posed upon the workers. When the essence of capitalism is that the capitalists are the risk takers. Now the trouble is capitalists are risk takers but the financial sector is behaving like a parasite and dumping its failures upon the future incomes and retirements of working Americans.”

Contrary to popular belief there are no black swans. There are just people who ignore the lessons of history. Today, the key to survival is studying history and ignoring the herd.

While the herd waits for data points, the smart money has resisted, knowing that the only thing data points indicate are the most recent trends. When we do look to history we see that only those who’ve maintained their individuality in the face of mania are the ones who stand to make the biggest gains when the herd finally turns.

We’re standing on the cusp, arguably the knife edge of a massive trade war. President Trump says he’s going to impose all these tariffs and all the rest of it. Will that happen? Is that just him doing some marketing on Twitter? And if it does happen, what happens to the global economy?

Feierstein tells Renegade Inc. that the thing about Trump is you know a lot of his stuff is bravado and bluff and it seems to work fairly well.

“Do I think that there need to be changes and adjustments? Absolutely,” he says. “But I still think that the EU will not exist in its current form within the next three to four years. There’s going to have to be a major structural change because countries like Spain, and Italy and France are not happy with the way things are rolling.”

When Jean-Claude Juncker, President of the European Commission, talks about thawing relationships with Russia, why is he saying that now? And why is he saying, look we have to stop demonising Russia in the way that America has done and the UK for as long as we can remember?

“I think Merkel’s pulling his strings,” Feierstein says. “Because I think Germany needs to realise that Russia is not really the bogeyman. Russia’s GDP is $1.2 trillion I think. It’s under $2 trillion depending on which metric you look at. It’s very small.

“Is Russia a risk? I don’t think that there’re a geopolitical risk, or geo-economic risk at all.

“I think that the biggest risk in the world is China. But nobody wants to talk about it because they have immense lobbying capabilities.

“So the old pay-to-play, the brown envelopes, and the politicians kept sweet by saying ‘hey look, we’ll take care of you, we’ll make sure you’re reelected’. And then the Hollywood scene where they decide what movies get get published, what movies don’t get published. So China I think is your biggest risk.

“I think that the reason Junker has come out and said he wants to normalise the relationship with Russia is because he wants to take a stick and poke it in Donald Trump’s eye. And because of the position that the Congress and America has taken with Russia Russia, Russia, Russia, Russia and so Trump said ‘I’m going to have sanctions against the EU’. So Juncker probably thinks that is the biggest stick he can come up with.”

Feierstein says the reason why is there so much Russia phobia in the US is the need to find somebody to demonise.

“The Russia Russia Russia thing: it’s a theme in television shows, it’s the boogeyman,” he says. “There’s a Russian under your bed. You’ve got to look in your closet.

“It seems to fit a political narrative because they wanted to defer attention. It’s the great Four D’s as I call it: divert, deflect, deceive and deny. So if you watch this over here, this is really what’s going on over here.

“They try to indoctrinate people through the media and condition them to say: ‘Oh, Russia must be bad. They need to have some kind of enemy to try to divert attention away from the changing economy, the opioid addiction in America. The other economic issues that nobody wants to talk about.”

Feierstein calls this the deep state at work.

“These are the the life time bureaucrats in America that are very dangerous to democracy,” he says. “Free speech is cut off. And now you’ve got these civil forfeitures, where they’ve found people with their life savings that they were taking to open a business and the police just take it away from them. If they find too much cash on suspicion, they can just take it away and you’ve got to go to court and it might take you years to ever get your money back. This is a problem with democracy and this is especially a problem in the United States.”

Is that happening because the underlying economic fundamentals aren’t in good shape and what we’re starting to see is this economic doctrine falling apart?

“Not so much the economic fundamentals, as the country is broke pretty much,” says Feierstein. “If you look at how much debt the United States has accrued, it’s probably north of $250 trillion, which is almost four or five times global GDP. So they’ve got to figure out a way to make money, or to raise taxes which can’t be palatable right now because if they raise taxes it’s going to kill the economy. So they’re cutting taxes which is going to create bigger, fundamental problems down the road.

“The unemployment numbers which the government claims are below 4% are bogus because you’ve got close to 100 million people that are not participating in the economy.

“So if you are on the unemployment rolls, whenever you fall off those rolls you’re no longer counted as unemployed, you just don’t exist anymore.

“Obviously those numbers are going to go down because those people just aren’t counted any longer.”

For democracy to function properly you need a very well established and a very efficient fourth estate, i.e: media, to hold power to account, to flag up the truth and to keep elected leaders honest, if that’s possible. What has happened to media in the US?

“This term that I’ve been talking about for years, I mean a lot of the reporting by traditional media is ‘fake news’. It’s a propaganda narrative. He who controls the media controls the people. A lot of people because they see it on TV they say, ‘oh this must be true. I saw it on TV’. Is it true? Of course it’s not true. Look, you’ve got to go out and do your own research. But what you’ve got to look at are all the warning signs and whose interest does it serve for them to come up with a narrative?”

Feierstein says the media, Washington and the public are suffering from Trump Derangement Syndrome.

“There’s a group of people that really don’t care about anything except get rid of him, impeach him, get him out of office at any cost, no matter what.

“And we’re willing to accept tyranny as a result of that,” he says.

“Which is in effect what people are trying to do. I told you Trump would be elected. I was one of the only people that predicted his victory, even when the New York Times and The Huffington Post said 99% Hillary is going to get in. I said what you don’t understand with all this, what they do is they demonise like they do to Russia. The same thing with Trump. That’s why they created as the first narrative that he was beholden to Putin himself. He was in his side pocket, so he must be bad. And then that fell apart and it didn’t work, so now they’re saying, well he colluded to fire somebody who he was allowed to fire. So you know, they come up with something different each time that people will buy.

“But you’ve got you’ve got to realise that this is an issue. It’s not a conspiracy theory. This is actual reality happening. If you look at the narrative that they’re pushing, the reason why they do that is because people want to hear it. It feeds populism.

“The reason why I said he would win the election is because people are fed up with being lied to by the media. So what’s happening is the media right now is getting less and less credible. And people are starting to not listen to them anymore.

“But if you look, the United States as a whole, and I said this before the election, and this is why I said Trump would win and this is why I said Brexit would happen. This is just the beginning. What’s happening is you have a bubble in New York and you have a bubble in California and these guys control the media basically with groupthink.

“Like Jack Dorsey at Twitter decides who is popular and who isn’t. They have algorithms that control that. I wrote an article about Facebook, Google and Twitter being evil. And they are. And so is Amazon. I mean they have far too much power and they own pretty much the pay-to-play swamp in Washington. And this is a bit of the control. Google controls what you see when you when you hit a search.

“Everything is being controlled and monitored. This is not social media. It’s social control.”

Feierstein has been very bearish and negative on real estate, certainly in the UK. He says

real estate should always be purchased as an asset, but not an asset class.

“The way that you differentiate between an asset and an asset class is, property lacks liquidity. So in times of stress, an asset class you can always buy and sell buy. But if you own a property valued at £1 million or £2 million, there’s going to be no buyer, even at any price. Maybe £100,000. So that’s why I don’t consider it a liquid asset class where you can trade in-and-out of it.

“So when you buy a property, it’s not a speculative item, it’s poor man’s leverage. They’ve been able to get mortgages on a ridiculous amount of money relative to their income.

“As I’ve said, house prices have to be correlated to income for you to be able to pay your way. And if you look at the inflation numbers, what they’ve done now because house prices have escalated to bubble peaks, they don’t include the shelter factor in as much as they should, because if they did, inflation would be a lot higher than the numbers that they’re portraying inflation to be, which is a gigantic problem.

“Prices can go down just as easily as they can go up. They’ve only gone up because the central banks have manipulated this game. The problem is going to be when people have negative equity and they won’t ever be able to get out of this trade.”

Why is the West looking around the world for a war?

Has the time come for the people of West Asia to reclaim political and media narratives stripped from them by Western imperialism?

Are the chickens finally coming home to roost for the BBC?