Published: 29 May 2017

Guests: Rana Foroohar

Further reading: Makers and Takers: The Rise of Finance and the Fall of American Business

Most people who work in developed nations know that there’s something badly wrong in their economy even if they can’t fully articulate it. Many people feel they have to work harder and longer just to stand still. There always seems to be an economic headwind that denies fair return on the hours we put in.

So what is this formless force that pushes against us? And why is it such a different story for people who work in the financial industries who after such collective failure in 2008 are once again squeezing Main Street for every penny?

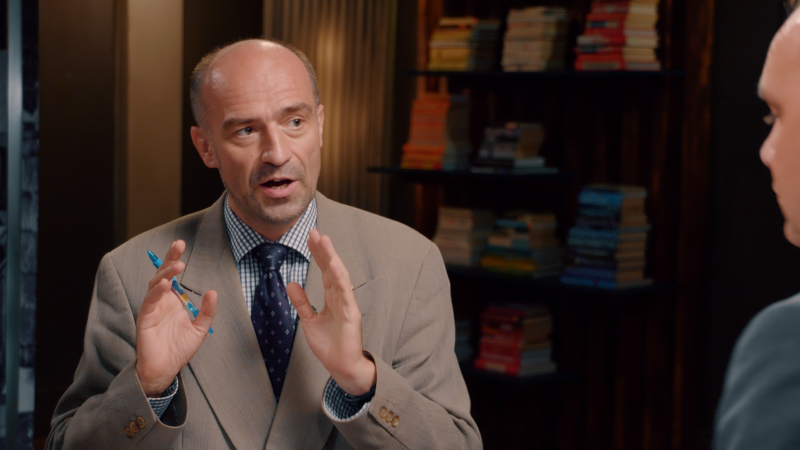

Host, Ross Ashcroft, met up with Author, Rana Foroohar, to discuss.

In her book, Makers and Takers, Rana Foroohar carefully outlines the important divide between, on the one hand, fund actualized industries whose business models mean they’re incentivized to take, and on the other, those in the real economy whose business models mean they actually have to make things for a living.

The makers could survive without the takers but the takers would find it much trickier without the makers. This means these two contradictory groups don’t make happy bedfellows. By clearly making this distinction, Foroohar has made an important contribution for anyone who intuitively feels that the financialization of our economies has come at a massive price.

Foroohar explains that what she sees when looking at the business landscape of division today, is a false narrative predicated on an Anglo American centric notion that what is good for business is good for consumers, workers and society at large.

The author points to data which shows that over the last 20-30 years, particularly post-crisis, there’s been an increasing disconnect between the fortunes of companies and the fortunes of consumers and workers. The extent of the divide is such that, in reality, the prosperity of the markets have no meaningful bearing with what’s happening on the ground. What’s good for business is not at all good for the average person in the developed world.

Foroohar describes the ideas which led to the writing of her book as a ‘come to Jesus moment’:

“In 2013, I was sitting in an off the record meeting with a former Obama administration official who had been involved in the bailouts of the too big to fail banks. We were talking about the Dodd-Frank financial regulation. And the official is saying, ‘well you know banks have not been able to manipulate this process. We have gotten stronger regulation through’. I had just done a column set noticing that 93 percent of all the meetings on some of the most contentious parts of regulation had been taken with bankers themselves, the institutions and individuals who were going to be regulated.”

Foroohar continues:

“I raised my hand and I said, ‘well how can you say that you’ve gotten a great piece of regulation through when 93 percent of the people talking about it are the ones that are going to be regulated? He looked at me with really honest befuddlement and said, ‘well, who else should we have been talking to? And I remember looking around the room which was filled with financial beat reporters and thinking, oh my gosh everyone’s going to be scribbling and no one was. There’s so much cognitive capture, conventional wisdom and such a narrative that nobody even understands. How bizarre that is.”

What Foroohar expresses in the above quote, is the inability of corporate ‘insiders’ to analyse in a dispassionate way the system in which they operate due to the fact that they are embedded within it. Indeed, the author points to research which indicates a correlation between high education levels and the tendency to become fixated about a tightly held prejudiced worldview.

Foroohar, however, highlights an important cultural distinction that exists between old school financiers in their 80s like Warren Buffet and Jack Bogle who came of age when the financial system was very different, and the new breed of financier.

The former have a different perspective in as much as they see themselves as being stewards of people’s money as opposed to traders and they question whether some of the people involved in the crisis could have pushed back more on the banks.

Foroohar suggests that the reason why Barack Obama, who presided over the 2008 crisis, wasn’t as successful as he might of been in obtaining his domestic political agenda, was because his bailing out of Wall Street at the expense of Main Street meant that there was no positive shift in social indicators. This resulted in a vacuum of leadership.

Ultimately, Obama surrounded himself with a bunch of neoliberal economists who managed to persuade him that standing up for the value extractors was a more sound worldview than standing up for the value creators.

How we begin to shift the priorities of business towards actually serving society as opposed to extracting value from it, is an issue that concerns Foroohar. While promoting her book, the author recalls how she was approached by a group of artists to speak about rent-seeking housing issues because it embodied their everyday life experiences as part of the ‘Soho effect’ gentrification process.

People often think about housing and rent, but actually rent-seeking goes across the board, from executive pay to political culture. The financialization of housing through rent seeking, or anything else for that matter, is about monopolizing markets.

Foroohar highlights the extent of the financial sectors dominance. The author says that in the US, the finance sector represents 7 percent of the economy, creates 4 percent of all jobs but takes 25 percent of all corporate profits. The author says that many business people have expressed to her disbelief and stunned outrage that bankers take a quarter of all private sector profit.

“Interestingly”, says Foroohar, “corporations that are public tend to be part of that whole process because CEOs get anywhere from 30 to 80 percent of their pay and share options. So they play the rigged market game. They push up their share price quarter by quarter by buying back their own stock. We have a system of incentives that is pushing everybody in exactly the wrong direction.”

Foroohar has interviewed enlightened financiers at the high end who understand this game and see the futility of it because they’re the canaries in the coal mine:

“They are the first to see where the markets are going and understand that 40 years of fake financial sized growth will hit their portfolios. They’re trying to understand how we can get back to more creating and making at the ground level. People like Richard Bookstaber actually came out with a book saying what we need is to throw all of economics out the window because it simply does not account for the messy truth of human life.”

Here, Foroohar touches on what she said previously above about how, when really smart people get very entrenched in ideas, it’s very hard for them to let that go and group-think takes over. However, the author also remarks that there are others within the sector who are able to actually step out of this straight-jacket thinking and deploy large pools of cash to Main Street to help shift the dynamic towards a more transparent and localized financial system.

The problem – as Elizabeth Warren has noted – is that there has never been a meaningful conversation among top financiers about what business should be doing, how we talk about finance and what the social impact of it should be.

Foroohar says that the reason for this is that the lexicon of financiers is tribal in nature and intended to alienate the average person. However, particularly among the creative and artistic community, this is beginning to change. It’s this community of people who are arguably best positioned to shift the debate forward to something more meaningful and transparent.

It is within this context, the author argues that at the current historical juncture, there is reason to be optimistic about the potential for society to rise from the ashes of crisis into a bonfire of opportunity.

Author of Medici Money, Tim Parks, discusses the Medici banking dynasty and its legacy.

Has the pernicious creation of hero or saviour complexes derailed the collective good?

What are the consequences of immunity or vaccine passports and will these proposed temporary measures become the norm?