There is no other way to describe economics in 2017 than wilful blindness, writes economist Professor Steven Keen. Nobel Laureates who claimed financial crises were now impossible also claimed the 2008 Global Financial Crisis could not have been predicted. This is all, of course, nonsense. The evidence was there all along. Those with the power to change the course of history simply chose to ignore it.

The phrase “There are none so blind as those who will not see” normally turns up in religion, but there is no other way to describe the dominant sect in economics today as wilfully blind. One decade after the crisis, most still repeat their mantra that, though a Nobel Laureate had asserted in 2003 that such crises were now impossible, the one that occurred in 2008 could not have been predicted.

Nonsense. The data that showed what would cause the crisis, and arguments by empirically oriented economists, were available before it hit: there was a runaway bubble in asset markets caused by too much credit being created by the banks.

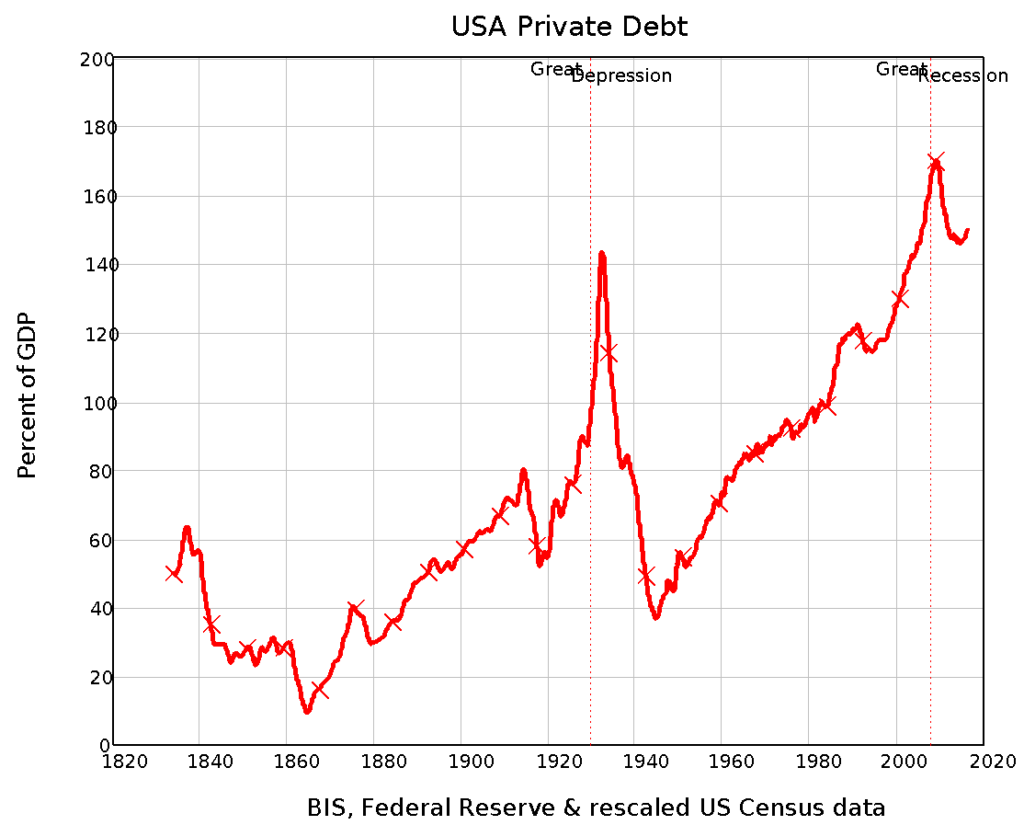

Credit—your capacity to buy something with money borrowed from a bank, rather than from your own cash—is exactly equal to the increase in private debt every year.

The bigger this is compared to GDP, the more the economy is dependent on credit; and the bigger the accumulated debt is when compared to GDP, the more likely it is that a reduction in credit will cause an economic crisis.

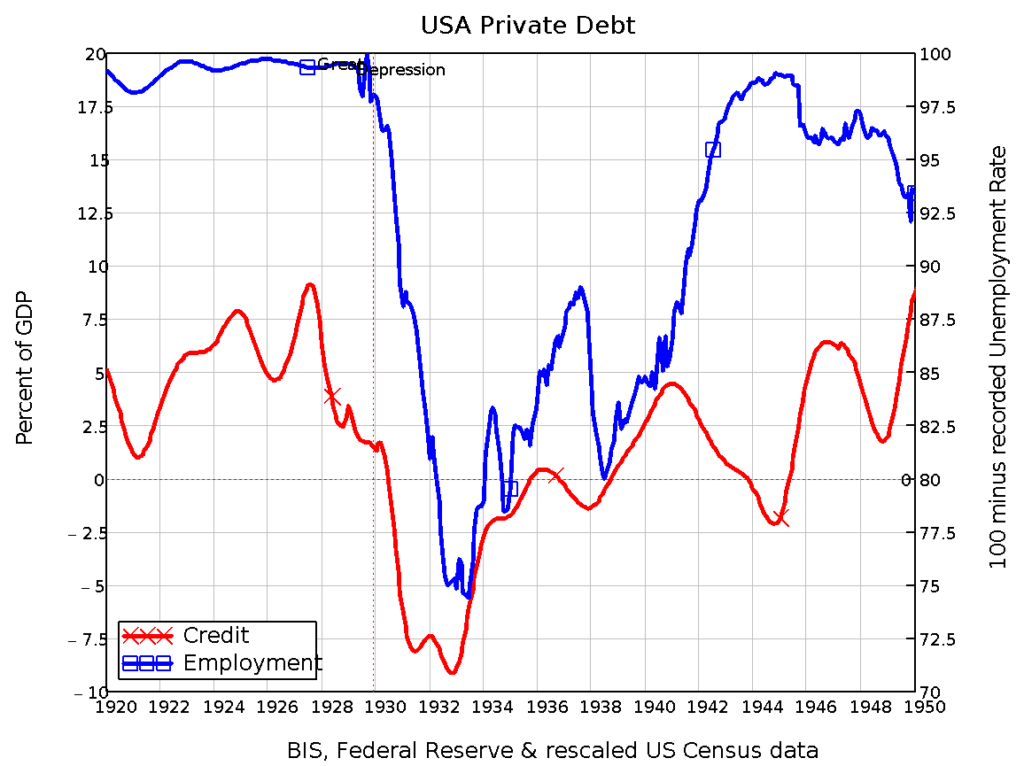

The data, if you look at it, is incontrovertible—especially if you consider the epicentre of the 2008 crisis, the USA, in historical context. The Great Depression was preceded by a margin-debt-fuelled bubble on the US stockmarket, with private debt blowing out during the crisis and then collapsing. That’s exactly what happened in the Great Recession.

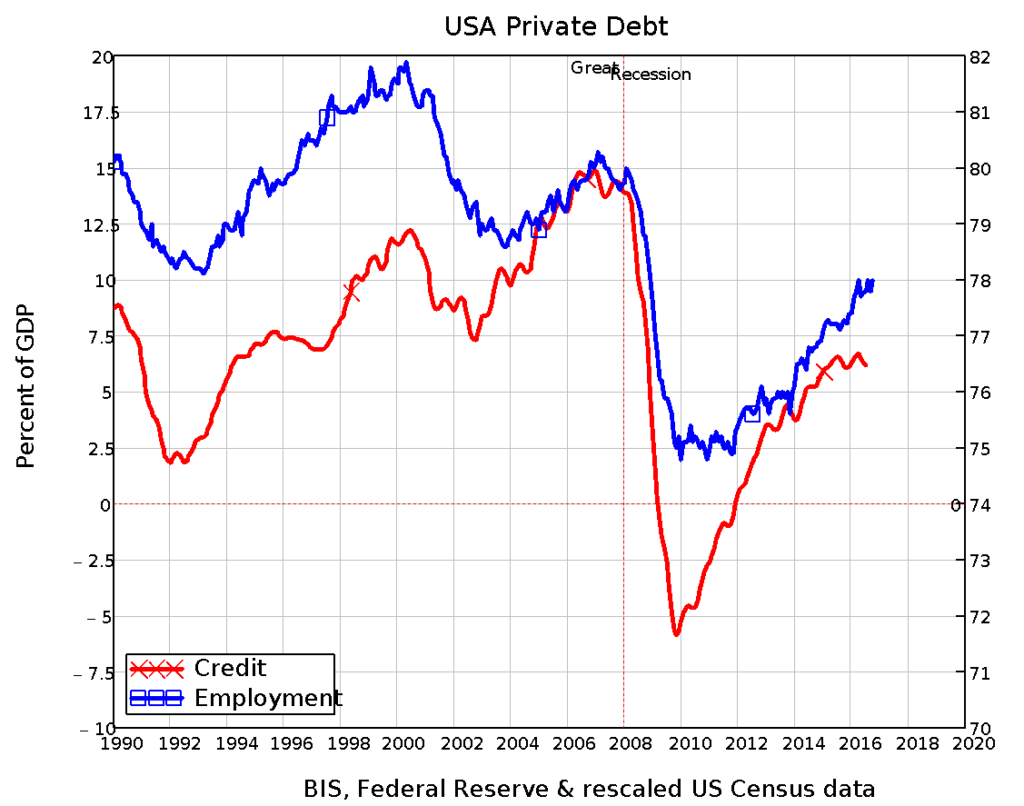

Private debt affects the economy in two ways: the higher debt is, relative to GDP, the more that a change in credit impacts on total demand. And credit adds to total demand by allowing people in the aggregate to spend more than just the money they currently have—with the price of leading to a higher level of debt in the future.

The correlation between credit and employment is staggering—not just because it is so big (the correlation coefficient, for those who follow these things, is 0.8), but because according to mainstream economists like Ben Bernanke, the correlation should be close to zero.

Bernanke, who got the job as Chairman on the Federal Reserve because he was supposed to be the expert on what caused the Great Depression, didn’t even consider similar data that was available at the time, nor the “Debt Deflation Theory of Great Depressions” put forward by Irving Fisher at the time, because he believed that credit was a “pure redistribution”, and “pure redistributions should have no significant macro¬economic effects” (Bernanke 2000, p. 24).

Empirically, this is manifestly untrue, but economists turn a blind eye (and not a Nelsonian one) to this data because it doesn’t suit their preferred model of how banks operate. They model them “as if” they are intermediaries who introduce savers to borrowers, not as originators of both money and debt. This deliberate blindness was, in a sense, excusable before the crisis, but it’s unforgivable after it—especially since Central Banks are actually coming out now and saying that this “Loanable Funds” model is a myth (here’s the Bank of England on the topic).

Central Banks have therefore learnt something from the crisis, but academic economists are, in the main, trying to go backwards to their defence that this crisis “could not have been predicted”.

But in fact it was predicted , by economists who take banks, debt and money seriously, like Ann Pettifor, Wyne Godley, and myself. Using the same analysis today, I don’t expect a crisis in the USA and UK in the near future, but rather stagnation like that which Japan has experienced since its “Bubble Economy” burst back in 1990. There will be revivals and reversals, but not an outright crisis because a pre-requisite for that is very high levels of credit. While the overhang of private debt from the last crisis persists, credit-based demand will be anaemic compared to pre-crisis levels.

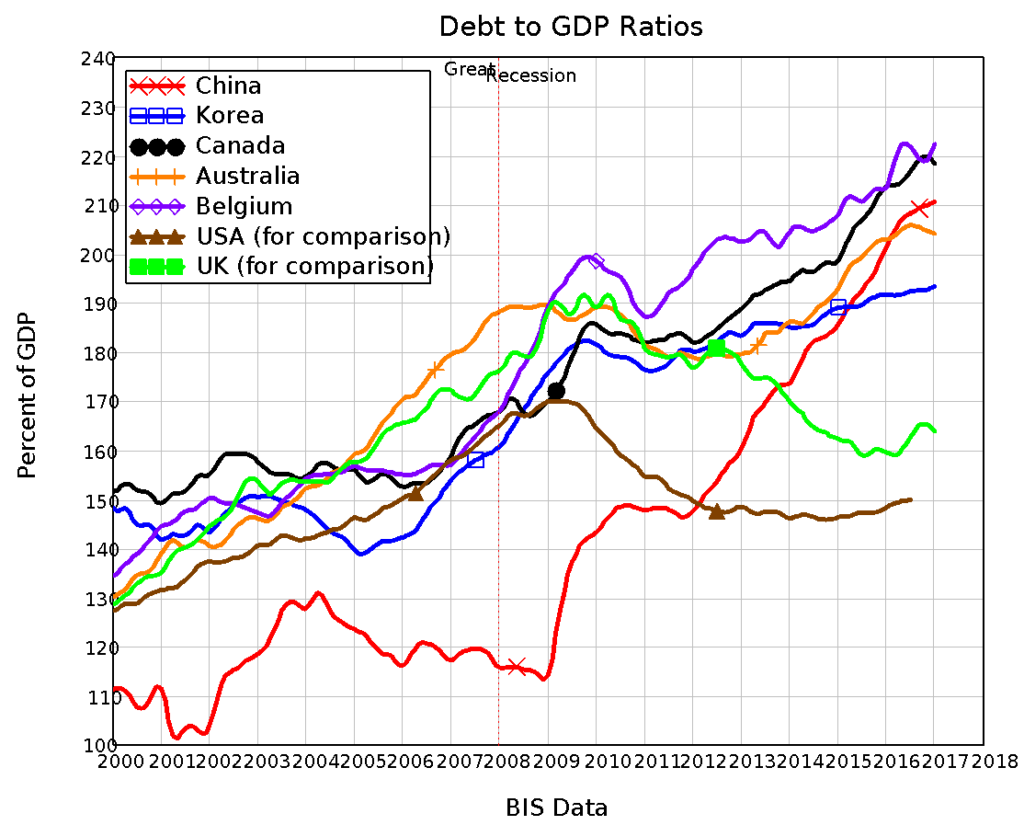

Instead, crises are likely in countries which side-stepped trouble in 2007 by continuing their private debt bubbles. The pre-eminent candidate here is China, whose credit bubble is easily the fastest growing in the history of capitalism; but it will have the company of South Korea, Canada, Australia, Belgium, and a number of other countries.

So there won’t be another Northern Rock in the UK or WaMu (Washington Mutual) in the USA, but that’s not thanks to economists, who continue to debate the largely symptomatic reactions of government debt to the rise and fall of private credit binges.

There is some hope: some prominent Neoclassicals are now doing some serious navel-gazing at their models, rather than resting on the “can’t predict exogenous shocks” defence (people like ex-President of the Minneapolis Federal Reserve Narayana Kocherlakota (Kocherlakota 2016), and World Bank Chief Economist Paul Romer (Romer 2016)). But more likely change will come from Central Bank, and the young students who’ve established the Rethinking Economics movement.

Reproduced with the kind permission of the author. To appear in The Conversation next week.

Bernanke, B. S. (2000). Essays on the Great Depression. Princeton, Princeton University Press.

Kocherlakota, N. (2016). “Toy Models.” from https://docs.google.com/viewer?a=v&pid=sites&srcid=ZGVmYXVsdGRvbWFpbnxrb2NoZXJsYWtvdGEwMDl8Z3g6MTAyZmIzODcxNGZiOGY4Yg. Romer, P. (2016). The Trouble with Macroeconomics.

Government and household budgets briefly explained.

Host Ross Ashcroft talks with the anthropologist David Graeber about Batsh*t Construction, a trend that has gripped the world.

Unless we start calling the housing crisis by its real name: extreme land monopoly - we’ll end up with ever more loony solutions for what should be a basic human right.