The Australian financial system is like a drug addict in denial, putting itself into ever increasing debt for overpriced property that most households will never be able to pay off.

Australian economic growth has occurred artificially, thanks largely to the mining boom, population growth and the finance, insurance and real estate boom. But growth in rents and income has not occurred along with it.

The country finds itself in a catch-22 situation where it cannot kick its addiction to private debt without severe withdrawal symptoms, to the extent that only another recession or Global Financial Crisis will force us to go cold turkey.

Recently, the media has focused on Australia’s household indebtedness, poor housing affordability and risks therein. Although policymakers have attempted to paint a rosy picture, rising household debts continue to cause problems.

Government and regulators are in a bind given the household sector has accumulated gargantuan debts but cannot be allowed to deleverage. Accelerating mortgage debts have boosted land prices to extreme levels, explaining why the nation has some of the world’s highest housing prices and household debts.

This had benefited the wealthiest into whose hands ownership of land and banks are concentrated. Reducing debts and hence land prices would diminish the generosity of the two most popular welfare payments in Australia: land rent and usury (bank loans). This capitalist welfare system is based on inverted principles; those who need it the least obtain the most.

Another reason why policymakers won’t halt debt accumulation is that debt issuance increases demand without reducing it elsewhere (the correct credit creation theory), as empirical research by economists Steve Keen and Richard Werner demonstrate. Even a slowing rate of growth subtracts from demand.

Put another way, our economy is like a drug addict. As the body becomes used to the drug, an increasing amount is required to achieve the same effect. With anaemic economic growth, policymakers cannot risk households deleveraging, which explains why the banking regulator APRA’s first and second rounds of macroprudential controls were very weak.

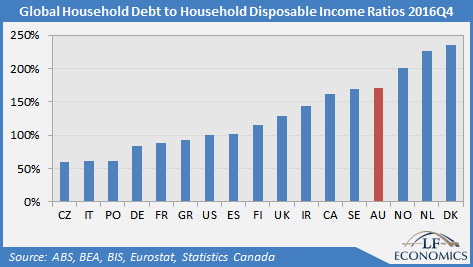

While the focus of household debt is in relation to GDP, household income is more accurate. Interestingly, all nations toward the higher end either have or had housing bubbles. In Australia’s case, this is unsurprising, given it currently has the world’s 2nd highest household debt to GDP ratio, the 3rd highest debt service ratio (DSR; measuring aggregate debt payments to income) and 4th highest debt to income ratio.

There is a sharp divergence in the growth of the household debt to GDP and income ratios. Rising exports have caused the growth in nominal GDP to increase to 8% while aggregate household income growth stagnates to 2% on an annual basis. The slack in the labour market, especially underemployment, is a primary contributor of weak income growth.

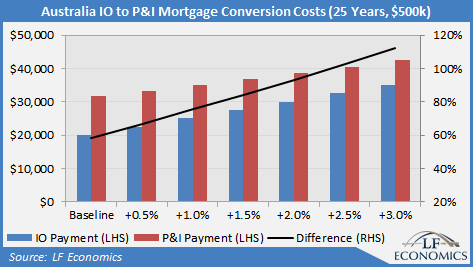

A risk for some households is the insistence of banks not renewing the interest-only period for mortgages. Such loans are typically reviewed after five years, and while banks have generally allowed renewals, this is increasingly not the case today.

The following figure demonstrates the rise in debt payments upon conversion from interest only mortgages to standard repayment mortgages at different interest rates for a hypothetical $500,000 loan at 25 years. At a rate of 4%, debt payments can rise by almost 60%, through to a smaller 20% increase at a rate of 7%. At present, households are paying an average of around 5.5% on their mortgages, implying an increase of 34%.

If conversion to standard repayment mortgages was to occur amidst rising mortgage interest rates as some officials believe may occur in the coming years, debt payments would increase astronomically. The payments for a $500,000 mortgage at 25 years with a baseline rate of 4%, rising by 100bps to 5%, can jump by 75%. With a 200bps rise, payments double.

With interest-only loans of 25% for owner-occupiers, 66% for investors and 39% in total, relative to the stock of total mortgage debt, conversion would present risks to overleveraged borrowers, even if the interest rate on P&I loans are slightly lower than for IO loans.

With the last round of productivity-enhancing policies implemented back during the 1980s, successive governments have relied on the mining boom, the FIRE (finance, insurance and real estate) sector boom and extreme population growth to artificially grow the economy. As the economic stimulus from investment relating to the mining sector subsides, policymakers have only the latter two elements to rely upon.

At least the government is cushioning the private sector with its budget deficits, but both sides of politics still believe aiming for a surplus is the correct policy measure. It is frightening in this day and age that economists and politicians have yet to figure out what public surpluses do to the private sector, especially in the face of persistent current account deficits.

Economists have also yet to understand that it only takes a tiny percentage of mortgages to become non-performing to topple banking systems, as central bank research indicates. Focusing on the aggregate, median or average borrower is misleading as it is the small number of overleveraged borrowers at the margin that generates systemic risks.

Unfortunately, the political economy has mutated to such an extent it is impossible for policymakers to reverse the economy’s addiction to private debt without causing severe withdrawal symptoms. It appears the nation may have to wait till the next recession or GFC 2.0 to deal with our problems, cold turkey style.

Philip Soos and Lindsay David

Lindsay David is the author of Australia: Boom to Bust, and Print: The Central Bankers Bubble. He recently founded LF Economics and holds an MBA from IMD Business School.

Latest posts by Philip Soos and Lindsay David (see all)

- The ghost of Gann: Another crash is coming - December 22, 2017

- Australian Housing Affordability the Worst in 130 Years - July 26, 2017

- Australia: A Drug Addict In Denial - July 4, 2017

Great post. I was checking constantly this blog and I’m inspired!

Extremely useful info specifically the ultimate part 🙂 I take care of such info much.

I used to be looking for this particular information for a long time.

Thank you and good luck.